John Sciulli/Getty Photos Leisure

I first talked about WM Know-how (NASDAQ:MAPS) to the In search of Alpha readers in mid-January, suggesting it could possibly be the most effective biotech and healthcare shares in 2023. The inventory then was $1.15, up about 14% year-to-date. Since then, the inventory has rallied, whereas the SPDR S&P Biotech ETF(XBI) has dropped 17%. The Well being Care Choose Sector SPDR ETF (XLV) has dropped 3.5%, and the New Hashish Ventures World Hashish Inventory Index has declined 11.2%. So, MAPS is doing higher than friends.

At first, although, it didn’t. The inventory set a brand new all-time low in April close to $0.60, down about 40% year-to-date. I added a bunch to my mannequin portfolio on the funding group that I run, and I additionally shared a chunk close to the start of Might suggesting that traders listen and that it was almost 9% of my hashish mannequin portfolio. It was then $0.71, so it’s up rather a lot now.

The inventory posted a 2023 excessive close to the start of September, and I ended up exiting my place because it moved larger. Final week, I loaded up once more at a median buy worth of $1.24, and it’s presently 7.7% of the mannequin portfolio. I’m very lengthy ancillary shares, and MAPS is third-largest from that sub-sector. I just lately wrote a few inventory that I like extra, Hydrofarm (HYFM), which is my largest ancillary place proper now. The inventory at the moment in early September was $1.18 and is presently up somewhat from then however down year-to-date.

On this piece, I have a look at the financials for MAPS throughout the first half of 2023, present an up to date analyst outlook, assess the valuation, and study the chart.

A Have a look at the MAPS 2023-H1

MAPS reported its Q2 in early August. Analysts, based on Sentieo, have been anticipating income of $48 million with adjusted EBITDA of $4 million. Income was larger than anticipated, falling 13% from a yr earlier to $50.9 million. Adjusted EBITDA was additionally higher than anticipated, at $10.2 million in comparison with a lack of $0.6 million a yr earlier.

For the primary half, income fell 15% to $98.9 million. The year-to-date adjusted EBITDA has been $17.4 million, up from -$1.5 million within the first half of 2022. The corporate has generated $4.1 million in money circulation from operations. It ended Q2 with no debt and $24.6 million in money. It additionally reported tangible e-book worth of $42.9 million.

The Outlook

Forward of the Q2 report, analysts have been anticipating 2023 income to be $193 million with adjusted EBITDA of $19 million. For 2024, they have been projecting income of $206 million with adjusted EBITDA rising to $25 million.

Now, analysts mission that income in 2023 will decline 10% to $194 million with adjusted EBITDA larger at $24 million . For 2024, they’re anticipating income will enhance 7% to $207 million with adjusted EBITDA of $27 million.

I’m utilizing 2025 estimates to kind a goal a year-out, and the analysts presently mission that income will enhance 9% to a file $225 million with adjusted EBITDA rising to $30 million, which continues to be beneath the 2021 stage and a margin of 13.5%.

Not solely do the margins appear to low, however I feel that the corporate will do a lot better than anticipated if their prospects are in higher form financially, which could possibly be the case if the 280E tax goes away.

The Valuation

After I wrote in Might, I shared a goal for year-end based mostly on 30X projected adjusted EBITDA for 2024, which was $3.26. In early August, forward of the Q2 report, I shared with my subscribers a revised goal of $1.94, based mostly on 2X projected income for 2024. That is nonetheless potential in my opinion, however I’m sharing in the present day a goal for a yr out based mostly on that very same a number of of 2X projected income for the enterprise worth. This calculation makes use of 75% of the 2025 estimate and 25% of the 2024 estimate.

The projected income two years out from now, then, is $220.5 million, which ends up in a focused enterprise worth of $441 million. I’m utilizing $20 million of web money to get a $461 million market cap, which suggests a inventory worth of $2.04, up 65%. This is able to be 15X projected adjusted EBITDA, which appears achievable.

The Chart

The inventory is manner down from the place it was forward of the Q3 report two years in the past:

Charles Schwab

Primarily based on this long term perspective, I see resistance close to $2.25, which is above my one-year goal. I see help close to the lows from earlier this yr at $0.60.

Wanting on the one-year chart, the inventory is off of the low, however additionally it is manner decrease than the height a yr in the past:

Charles Schwab

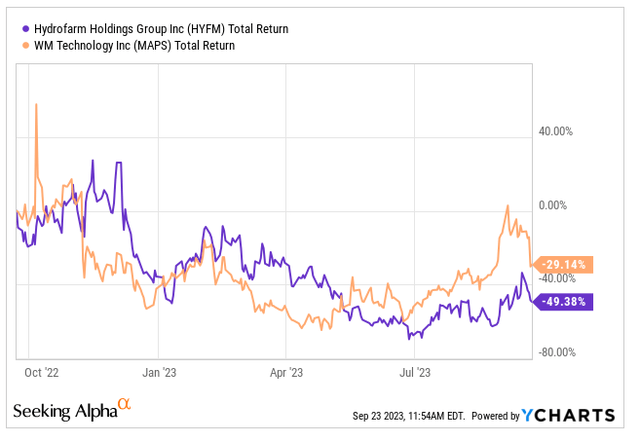

I discussed above that HYFM is a bigger a part of my mannequin portfolio. My goal in early September for HYFM a yr out was $3.59, which is up 194%. This can be a lot extra potential upside than I see at MAPS, however, as I mentioned in that piece: Hydrofarm has lots of web debt. Right here is the one-year chart evaluating the 2 shares:

YCharts

Each bottomed out at related ranges from the place they have been in late September a yr in the past, and MAPS is main the 2 shares larger initially.

Conclusion

MAPS is working! I feel it has a lot much less draw back threat than the MSOs if issues do not play out with 280E going away, and my goal may very well be too conservative. I do prefer it, however I want HYFM presently.

Buyers might actually like or dislike the to-be-named CEO. The present CEO, Doug Francis, is the Govt Chair, joined the corporate in 2009 and could be very skilled. MAPS has an interim CFO too. So, the administration workforce is a threat that traders ought to think about.

This inventory was cherished by hashish traders, however there’s not a lot signal of that constructive sentiment lately. I feel the inventory can do higher, and it may soar if its enterprise have been to choose up.

Editor’s Be aware: This text covers a number of microcap shares. Please pay attention to the dangers related to these shares.