Morsa Pictures

Veris Residential, Inc. (NYSE:VRE), integrated in 1994, is a REIT primarily engaged within the acquisition and administration of Class-A multi-family properties primarily positioned within the Northeast.

Though the REIT is in a turnaround course of, its leverage/liquidity points alongside with the very unattractive dividend yield and honest valuation make it too dangerous to purchase proper now. In case you are in search of an goal evaluation of VRE, on this put up I’ll current each the nice and unhealthy issues in regards to the firm that can assist you perceive why it is best in case you simply add it to your watchlist for now.

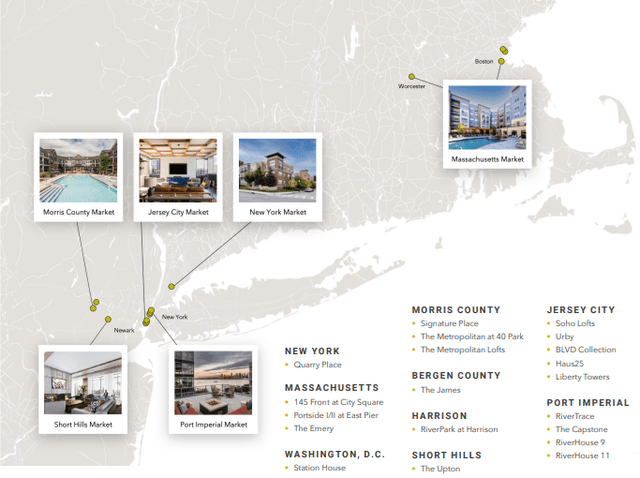

Portfolio

As of the third quarter, the REIT owned or had pursuits in 30 properties which consisted of 24 multifamily rental properties containing 7,681 residence models. It additionally owned developable land parcels and non-core belongings comprised of 4 parking/retail properties and two workplace properties.

The portfolio is unfold throughout New Jersey, Boston, Suburban New York, and Washington, D.C.:

Investor Presentation

Although the properties are usually not as diversified as these of different bigger REITs, they take pleasure in being in enticing places and providing resort-like facilities, comparable to state-of-the-art health facilities, canine parks, lounges, clubrooms, and rooftop swimming swimming pools. Furthermore, they’re 6 years outdated on common, which suggests much less upkeep bills than these older belongings of many residential REITs require.

You also needs to know that within the final 3 years, Veris dispositioned greater than $2 billion of non-strategic belongings, together with 25 workplace properties and two inns, as a part of its effort to grow to be a pure-play multifamily REIT, introduced again in 2021.

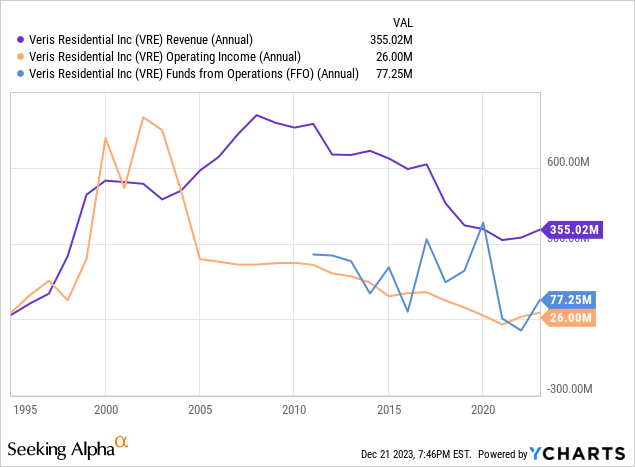

Efficiency

First, in the course of the third quarter, occupancy and retention charges have been 95.5% and 55%, respectively; sufficiently excessive for a residential REIT.

Nonetheless, the corporate’s working efficiency has been very erratic, making forecasts much less predictable:

The above chart would not inform the entire story although. That is as a result of income, working earnings, and funds from operations seize losses incurred by non-core belongings which Veris intends to eliminate. The identical-property money NOI coming from the multifamily portfolio has skilled quite a lot of progress. The final quarter’s determine annualized is 109.25% larger than the typical annual one of many final 3 fiscal years.

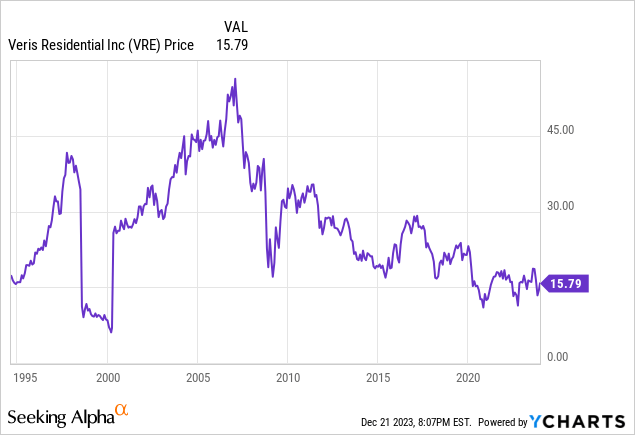

As you must count on, the long-term historic working efficiency has been adopted by a falling inventory worth:

Is that this deserved? Most likely. Is that this reflective of future efficiency? That is the place it will get tough as a worth development may be moderately used to foretell the longer term provided that the potential drivers behind the development are prone to stay current. A turnaround story is unfolding as you’re studying this, so the above chart ought to be taken with a grain of salt.

Leverage

As for Veris Realty’s monetary well being, issues look simply as unhealthy. It at the moment funds its belongings with 57.6% debt, has a debt-to-EBITDA ratio of 13.44x, and the curiosity protection sits at 0.16 instances.

So, though leverage is not dangerously excessive, it is excessive in relation to the REIT’s profitability, which in flip suggests insufficient liquidity.

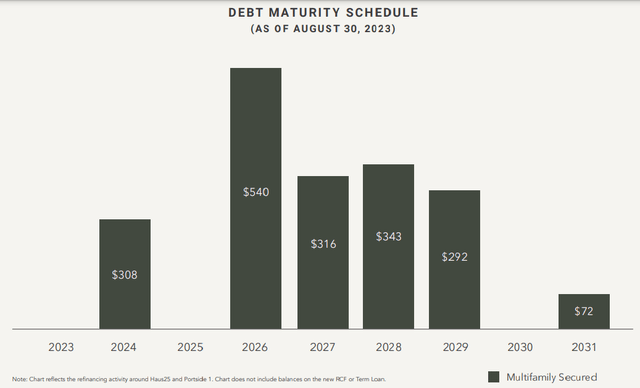

In distinction to this grim scenario stands the weighted common rate of interest of the corporate’s debt at 4.49%, which may be very enticing. And so is its near-term maturity schedule, with 16.1% of its debt maturing subsequent 12 months and nothing coming due in 2025.

Investor Presentation

Sadly, the low price of debt and no threatening maturities within the brief time period can’t overshadow the liquidity subject.

Dividend & Valuation

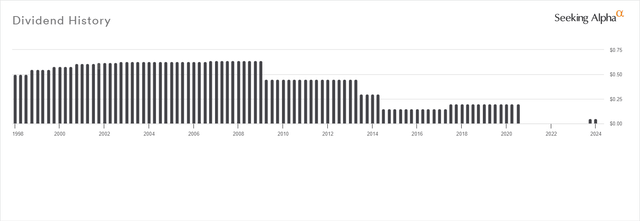

Veris Residential at the moment pays a quarterly dividend of $0.05 per share, which suggests a really unimpressive ahead yield of 1.26%. The low distribution is no surprise, contemplating that profitability is struggling. And the identical applies to the truth that the REIT began paying a dividend once more solely not too long ago at a a lot decrease determine than earlier than after suspending it in 2020. The truth that the REIT has been frequently decreasing it up to now can be in step with its money move issues:

In search of Alpha

What’s shocking, nevertheless, is that VRE is buying and selling at a 4.98% implied cap price, which roughly makes it pretty valued. I might count on that the market would provide the inventory at a reduction to NAV. Additionally, contemplate that it is truly overvalued on a peer-relative foundation with the median implied cap price being around 6% for residential REITs.

Dangers

This brings me to the primary danger associated to purchasing shares at honest worth or, worse, at a premium. The shortage of a margin of security may end up in a scarcity of conviction in your funding choice, which in flip may result in realizing a loss if the value falls much more sooner or later.

On the identical time, it is not useful that the corporate is not worthwhile sufficient to cowl its curiosity obligations. Even when that and its ever-increasing debt by no means drive it into defaulting, the market may reprice the shares accordingly if the scenario would not enhance.

One other however much less necessary danger pertains to the portfolio’s geographical focus. REITs are partly enticing to buyers as a result of they’ll provide a really broad publicity to markets throughout the nation. And justifiably in order this helps hedge dangers of inhabitants adjustments, unemployment charges, and adjustments in hire costs.

Verdict

Subsequently, I have to assign a maintain ranking to VRE for now and are available again to it if and when the issues I coated above are resolved. One thing not unlikely as we noticed within the portfolio part above; Veris Realty has already taken steps to grow to be a pure-play multifamily REIT and this may do it for it. We’ll have to attend and see as I believe it is manner too dangerous to purchase shares proper now. However VRE undoubtedly deserves an addition to your watchlist.

For now, it’s your decision to try an evaluation of Fairness Residential (EQR) that I wrote not too way back if you’re inquisitive about multifamily property publicity. Though it’s 12.85% up since then, the margin of security continues to be enticing and the dividend yield is way larger than Veris Realty’s.

What do you suppose? Do you personal VRE or intend to nonetheless? Let me know under and I will get again to you as quickly as I can. Thanks for studying.