After reporting a double miss for Q3 2023, Tesla, Inc. (NASDAQ:TSLA) inventory is down -3.5% to $234 per share within the after-hours session on the time of writing. Given Tesla’s recent delivery miss and collection of value cuts all through 2023, the weaker-than-expected monetary efficiency in Q3 was unsurprising. And, in my opinion, Mr. Market’s destructive response to Tesla’s incomes miss is justified.

Because the demand for autos has come below stress in a rising rate of interest surroundings, Tesla’s management has strategically prioritized unit quantity progress at the price of margins. Naturally, Tesla’s margins have compressed in current quarters, and the destructive development continued in Q3 2023. With auto gross margins of ~16.1% coming in effectively beneath avenue estimates of ~17.6%, Tesla is seeing a pointy contraction in free money flows, which narrowed to ~$0.8B in Q3. Whereas Tesla is the one worthwhile EV maker on the market, the corporate seems caught in a vicious pricing cycle, and pricing/margins [profitability] may come below additional stress in upcoming quarters if rates of interest stay larger for longer and the macroeconomic surroundings deteriorates from right here.

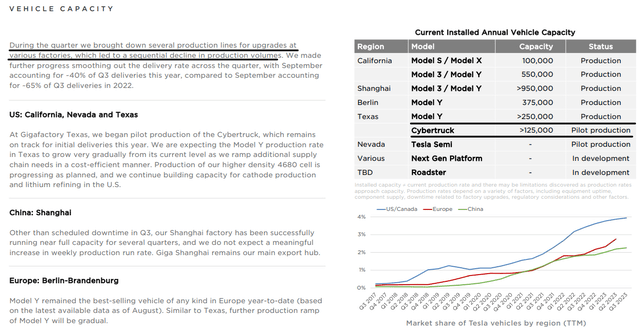

Curiously, Tesla’s administration appears to be hanging onto their 1.8M car manufacturing goal for 2023 [Q4 production of >470K] and Cybertruck deliveries are on monitor to start earlier than the top of this yr.

Tesla Q3 2023 Shareholder Deck

On this be aware, we’ll briefly evaluate Tesla’s Q3 2023 report and re-examine its technical setup. Moreover, we’ll check out Tesla’s absolute valuation (long-term danger/reward) to see if the inventory is a purchase, promote, or maintain within the $240s.

Reviewing Tesla’s Q3 2023 Report

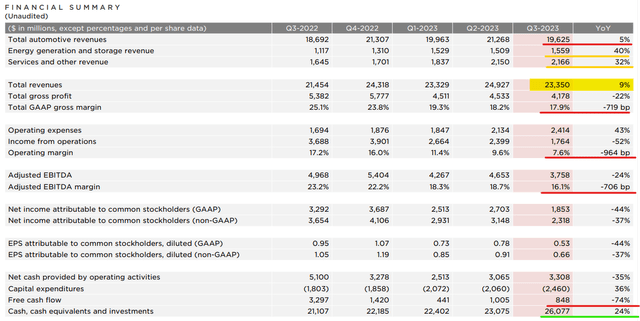

For Q3 2023, Tesla reported income of $23.35B and non-GAAP EPS of $0.66, lacking consensus estimates [revenue est.: $24.14B, EPS est.: $0.73]. As I shared in my Q2 2023 earnings evaluate:

Because of rising rates of interest, big-ticket objects like automobiles are inclined to get dearer for customers, and decreased affordability means decrease demand. So as to develop volumes by way of this era, Tesla has opted for aggressive value cuts during the last a number of months. And whereas these value cuts have enabled Tesla to stoke demand in a rising rate of interest surroundings, Tesla’s recession playbook is creating immense margin pressures.

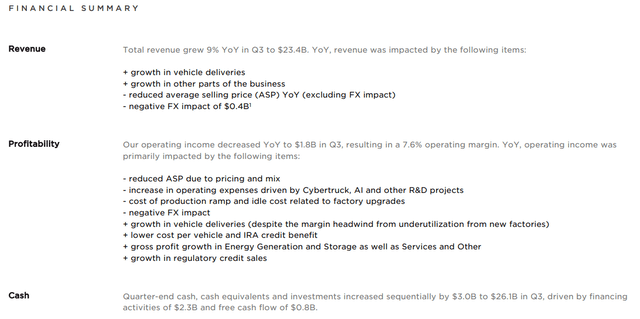

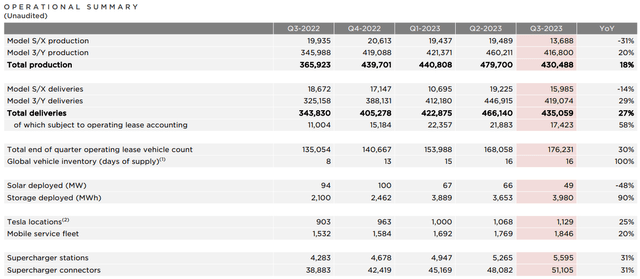

In Q3, Tesla’s GAAP gross margins fell to 17.9% (vs. 18.7% in Q2 2023) [below management’s guardrail of 20%]. Whereas decrease car ASPs and a shift in combine in direction of Mannequin 3/Y are hurting revenues and gross revenue margins (offsetting comparatively sturdy supply quantity progress of +27% y/y), a pointy enhance in working bills (+43% y/y) is driving a pointy contraction in working revenue and free money circulation manufacturing [down -74% y/y].

Tesla Q3 2023 Shareholder Deck

Tesla Q3 2023 Shareholder Deck

Throughout Q3 2023, Tesla delivered ~435K items (up 27% y/y) at a median promoting value of $45.1K [lower than the average price of a new car in the US]. In keeping with Tesla’s administration, the EV large continues to be on track to fulfill its 2023 car manufacturing aim of 1.8M items regardless of producing solely ~430K items in Q3 [pre-planned factory re-tooling outages].

Tesla Q3 2023 Shareholder Deck

Tesla Q3 2023 Shareholder Deck

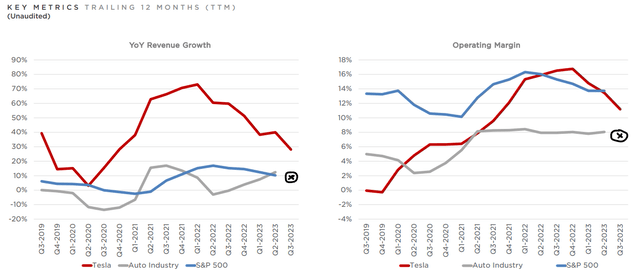

Regardless of nonetheless rising car deliveries at a speedy clip, Tesla’s income progress is decelerating quickly and profitability is deteriorating, with working margins nosediving in current quarters. As of Q3 2023, Tesla’s y/y income progress and working margins stood at 9% and seven.6%, respectively. And each of those key monetary metrics at the moment are beneath that of the common income progress and working margins for S&P 500 (SPX) firms and Tesla’s automotive business friends!

Given a pointy deceleration in income progress and cruel margin contraction, Tesla’s relative valuation seems utterly out of whack with actuality! Now, in my opinion, Tesla is not only a automobile firm, however given its auto-centric income combine and deteriorating margin profile, one might simply assume this to be the case. Actually, I would not be shocked if bearish buyers/merchants begin labeling Tesla as “simply one other automobile firm” in gentle of those disappointing Q3 earnings and name for a de-rating in TSLA to an auto inventory valuation.

Regardless of seeing the monetary logic behind this bearish argument, I proceed to imagine that Tesla’s actuality is someplace in between that of an auto and tech/AI firm. Here is what I’ve stated about TSLA up to now:

Whereas Tesla bulls might argue that TSLA deserves a premium as a result of sooner progress on the EV large and potential FSD-driven margin enlargement, bears would contend that Tesla is a CAPEX-intensive manufacturing enterprise with far decrease revenue margins in comparison with different massive tech firms. For my part, each bulls and bears have a defensible argument.

This stance is predicated on my understanding of Tesla’s futuristic generalized AI choices [FSD (autonomous driving) + Dojo (computing) + Optimus (humanoid robot)]. Sure, Tesla generates the majority of its revenues from EV gross sales; nevertheless, I believe there is a non-zero likelihood Tesla finally ends up constructing an enormous SaaS enterprise with FSD in the long term.

Here is what Musk stated in his opening remarks throughout Q2 2023 earnings name:

Within the long-term, autonomy we expect goes to only drive quantity by way of the ceiling subsequent stage. And our form of future robotaxi merchandise — devoted robotaxi merchandise we expect have like quasi-infinite demand. The way in which we’re going to fabricate robotaxi is, can be itself a revolution. So, it’s revolutionary design made in a revolutionary method. It’ll be by far the very best items per hour of any car manufacturing ever. So, very enthusiastic about that. With respect to Autopilot and Dojo, in an effort to construct autonomy, we additionally want to coach our neural web with knowledge from thousands and thousands of autos. The extra — I imply, this has been confirmed over and over. The extra coaching knowledge you will have, the higher the outcomes. And, I imply, there are occasions the place we see principally — in a neural web, principally it’s form of at 1 million coaching examples, it barely works; at 2 million, it barely works; at 3 million, it’s like wow, okay, we’re seeing one thing, however you then get like 10 million coaching examples, it’s like — it turns into unimaginable. So, there’s simply no substitute for an enormous quantity of information. And clearly, Tesla has extra autos on the street which can be amassing this knowledge than the entire firms mixed by, I believe, perhaps even an order of magnitude. So, I believe we would have 90% of all — or a really massive quantity. So, the success in AI endeavors is a operate of expertise, form of distinctive knowledge and computing sources. And we’ve excellent capabilities in all three arenas.

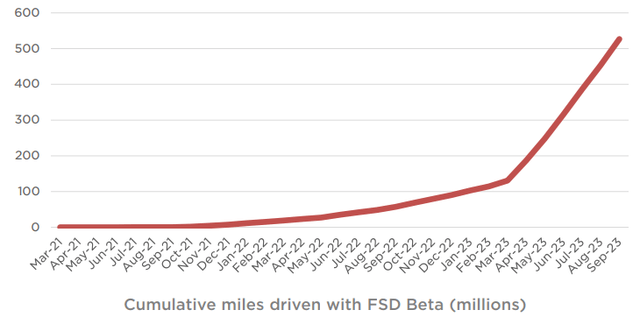

And I actually simply don’t know the way anybody may do what we’re doing, even when that they had our software program and had our pc, if they didn’t have the coaching knowledge. So, talking of which, our Dojo coaching pc is designed to considerably scale back the price of neural web coaching. It’s designed to — it’s considerably optimized for the sort of coaching that we’d like, which is a video coaching. So, we simply see that the necessity for neural web coaching — once more, speaking — talking of quasi-infinite issues, is simply monumental. So, I believe having — we count on to make use of each, NVIDIA and Dojo, to be clear. However there’s — we simply see demand for actually huge coaching sources. And we expect we might attain in-house neural web coaching functionality of a 100 exaflops by the top of subsequent yr. So, up to now, over 300 million miles have been pushed utilizing FSD beta. That 300 million mile quantity goes to appear small in a short time. It’ll quickly be billions of miles, then tens of billions of miles. And FSD will go from being pretty much as good as a human to then being vastly higher than a human. We see a transparent path to full self-driving being 10 occasions safer than the common human driver, so. And between Autopilot, Dojo pc, our inference {hardware} within the automobile, which we name form of {Hardware} 3, 4, however it’s actually devoted. It’s a excessive effectivity inference pc that’s within the automobile and our Optimus robotic, Tesla’s clearly on the slicing fringe of AI improvement.

Supply: Tesla Inventory: A Case Of Good Not Being Good Sufficient

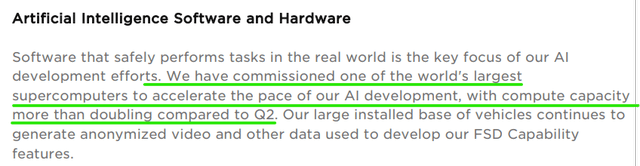

As we all know, Tesla has been creating every of the 4 principal know-how pillars wanted to unravel autonomy at scale in-house: an especially giant real-world dataset, neural web coaching, car {hardware}, and car software program. Tesla’s vertical integration benefit is what units it other than opponents within the race for autonomous autos, and I can see Tesla’s lead increasing within the close to future. In Q3, Tesla practically doubled its compute capability, with FSD Beta miles rising exponentially.

Within the Q3 earnings name, Musk talked about getting nearer to end-to-end autonomy with FSD 12.0 and reiterated the opportunity of Tesla changing into essentially the most precious firm on this planet powered by generalized AI – full self-driving (“FSD”) [autonomous driving] and humanoid robots. That stated, attaining full autonomy and getting over regulatory hurdles may nonetheless be a number of years out. In my thoughts, Tesla is popping right into a binary guess on FSD as a result of its harmful recession playbook (sacrificing margins to prioritize unit volumes), and Q3 2023 outcomes served as additional proof of this stance. Whereas FSD’s success is just not assured, Tesla’s future is closely reliant on it. Therefore, I will proceed to intently monitor progress on this entrance over the approaching weeks, months, and quarters.

As we all know, Tesla is already trying into licensing offers for FSD:

We’re very open to licensing our full self-driving software program and {hardware} to different automobile firms. And we’re already in discussions with — early discussions with main OEM about utilizing Tesla FSD. So, we’re not attempting to maintain this to ourselves. We’re more than pleased to license it to others.

Supply: Tesla’s Q2 2023 Earnings Name Transcript

Whereas I would like Tesla to construct a walled backyard akin to Apple (AAPL) if it solves FSD, I belief Musk and his management staff to maximise future free money flows for TSLA shareholders. And in the event that they imagine licensing FSD is the best strategy, I might make peace with that technique. Any bulletins on this entrance may have a big influence on Tesla’s inventory, which seems primed for an enormous transfer.

In Tesla Inventory: A $100 Transfer Is Imminent, I shared a cautiously bearish stance for TSLA with the inventory buying and selling at ~$270 on the time:

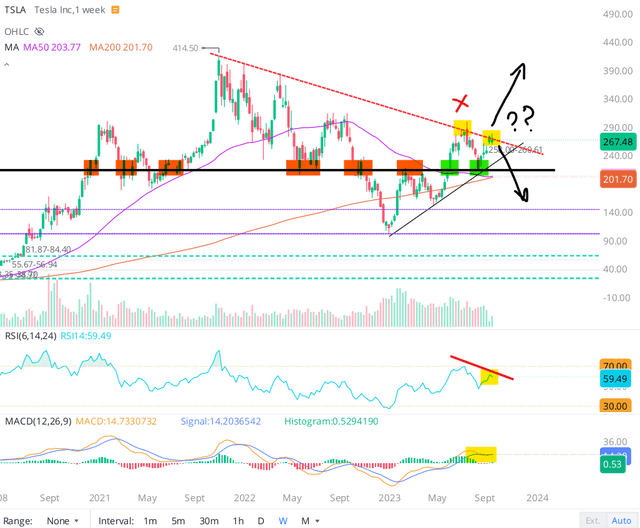

The bull-bear debate round Tesla being a know-how or an auto firm continues to rage on, with TSLA’s value motion getting tighter and tighter in a triangle formation marked within the chart beneath –

Tesla inventory chart 9/12/2023 (WeBull Desktop)

Listed below are the 2 potential paths I see for Tesla:

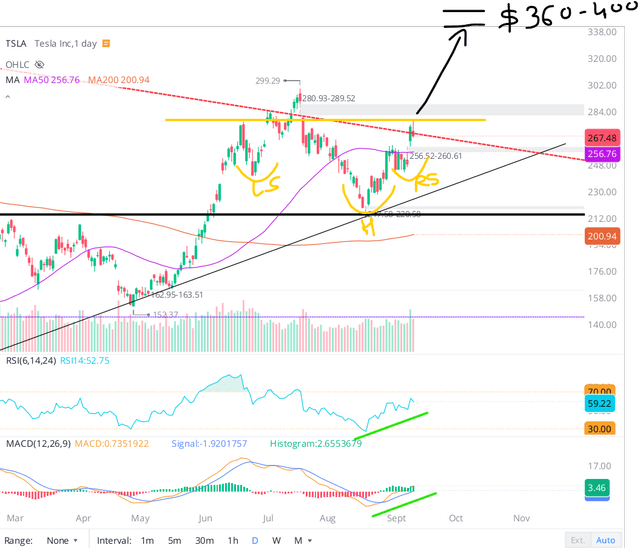

1) An upside breakout above the $280-300 resistance zone may affirm the bullish “Inverse Head & Shoulders” sample marked on the chart beneath:

WeBull Desktop

The value goal of this bullish “Inverse H&S” sample is ~$360, and if TSLA can retain bullish momentum, it may simply lengthen to new all-time highs above ~$400. For my part, an increase in each day RSI and MACD indicators since mid-August helps an upside breakout. TSLA inventory is just not overbought, and with 50-DMA effectively above 200-DMA, technical momentum continues to be trying sturdy right here.

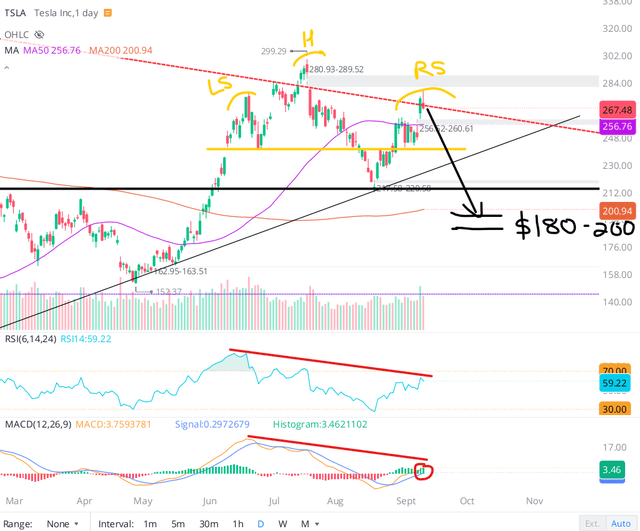

2) Conversely, a rejection at present ranges or the $280-300 resistance zone may simply ship Tesla shares tumbling again all the way down to the $240 (neckline) stage. And a breakdown of this stage would affirm the bearish “Head & Shoulders” sample marked on the chart beneath:

WeBull Desktop

The value goal of this bearish “H&S” sample is ~$180, which coincidentally occurs to be my honest worth for Tesla. Unfavorable divergence on each day RSI and MACD indicators since June helps a draw back breakdown. As of at the moment, each of those patterns are nonetheless in play, and Tesla inventory may transfer ~$100 in both route (up or down) when it breaks out of the huge triangle shaped on its chart.

From a technical perspective, TSLA inventory continues to be caught in no man’s land within the $215 to $280 vary, with danger/reward being finely poised at present ranges. Given the triangle formation, Tesla inventory may get away to the upside or break all the way down to the draw back within the close to future. Both consequence is feasible, however we are able to make sure that it’s going to be a giant transfer!

As of now, I might keep away from taking any new near-to-medium-term place in Tesla shares. Nevertheless, if I needed to take a place, it will be on the quick aspect with a good stop-loss. So, this hypothetical place could be “Quick Tesla at $270 (draw back goal: $180-200, reward: $70-100), with a stop-loss at $305 (danger: $35)”.

My rationale for having a cautiously bearish stance is kind of easy:

Tesla’s gross sales progress is decelerating and margins are contracting amid a tricky macroeconomic surroundings. With rates of interest more likely to stay larger for longer, and auto mortgage delinquencies on the rise, I count on auto costs to come back below additional stress within the foreseeable future. Whereas Tesla is main the auto business’s price-cutting train, such speedy margin deterioration isn’t perfect.

Given Musk’s recessionary playbook (prioritizing gross sales over income), Tesla is basically a binary guess on FSD attaining full autonomy (which can or might not occur).

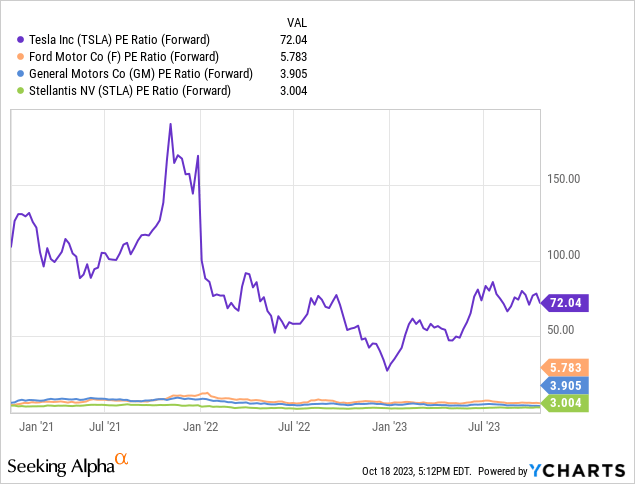

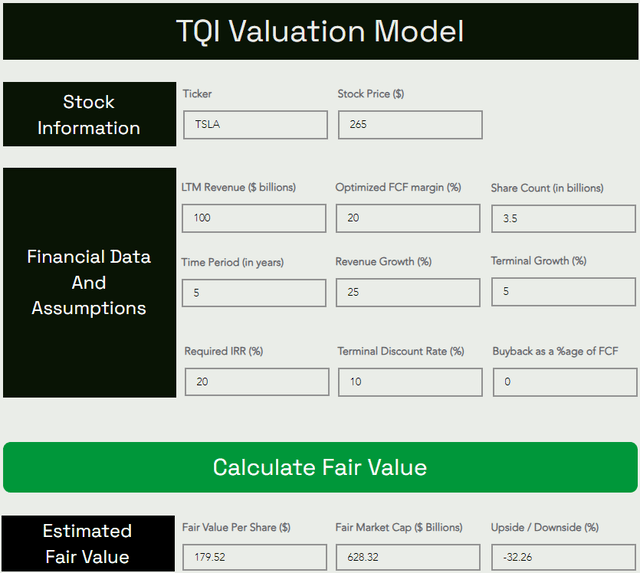

At >70x ahead P/E, Tesla carries a demanding valuation. In keeping with TQI’s Valuation Mannequin, Tesla stays overvalued:

TQI Valuation Mannequin (TQIG.org)

As per my mannequin, Tesla’s intrinsic worth is ~$180 per share. With the inventory buying and selling at ~$270 per share, it’s presently overvalued by ~30-35%. Now, I’m joyful to pay a premium for a high-quality firm like Tesla; nevertheless, the chance/reward is not enticing sufficient to justify an funding right here.

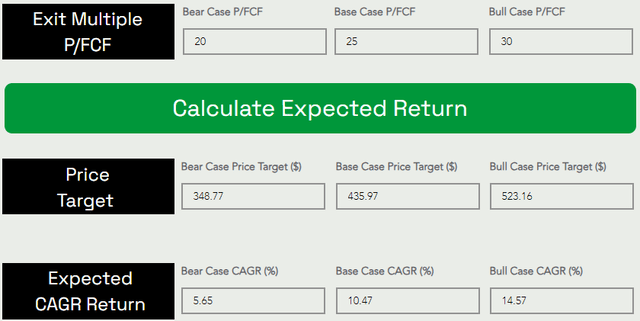

TQI Valuation Mannequin (TQIG.org)

Assuming a base case P/FCF exit a number of of 25x, I see Tesla hitting $436 per share by 2027. As will be seen beneath, Tesla is projected to ship CAGR returns of ~10.5% for the subsequent 5 years, which falls effectively in need of my funding hurdle fee (min. required IRR) of 15%.

With all of this stated, I’m not compelled to take a brand new place in Tesla inventory. Additionally, I do not quick particular person names ever, so establishing a brief place in Tesla is just not even a contemplation for me.

From a long-term danger/reward perspective, one would possibly argue that purchasing Tesla with an anticipated CAGR return of ~10% is okay. And perhaps it’s advantageous for some buyers; nevertheless, I’m laser-focused on long-term danger/reward, and TSLA failing to fulfill my funding hurdle fee of 15% renders it a “Maintain” for me at present ranges.

As you could know, I maintain an extended place in Tesla [accumulated in late 2022: Tesla Stock: An Asymmetric Buying Opportunity Arises Out Of Insider Selling, Demand Concerns, And A Scary Recession Playbook]. And as of now, my plan of motion for Tesla hasn’t modified:

If we see a fast transfer to the $360-400 vary, I’ll e book partial income on my lengthy place.

Conversely, if we drop all the way down to $180, I’ll restart accumulation and add to my lengthy place.

Supply: Tesla Inventory: A Case Of Good Not Being Good Sufficient

Key Takeaway: I proceed to fee Tesla “Impartial/Maintain” at ~$270 per share.

Supply: Tesla Inventory: A $100 Transfer Is Imminent (September 2023)

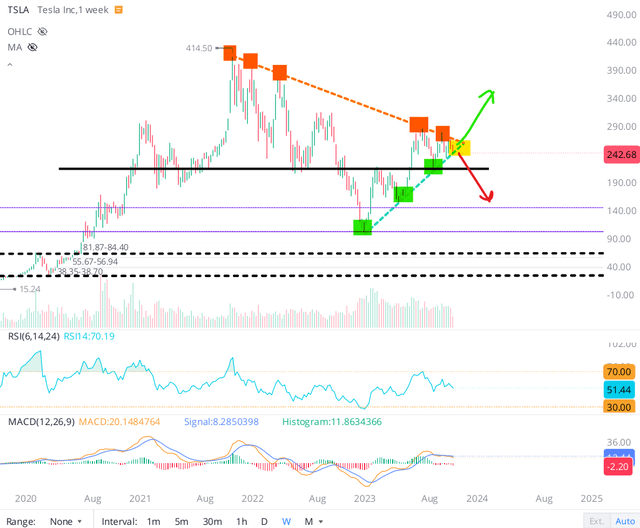

As of at the moment, Tesla inventory stays caught smack in the course of the $215 to $280 no man’s land, with the worth motion getting tighter. As I see it, Tesla is a coiled spring prepared to interrupt in both route:

Tesla inventory chart (10/18/2023) (WeBull Desktop)

If TSLA regains the $280 stage shortly after which manages to interrupt above the current excessive of ~$300, I can see a run-up to the $360-400 zone. On the flip aspect, a breakdown beneath $215 would open up a transfer all the way down to the mid $100s. With the chance/reward finely balanced (100-140 factors up and ~60-100 factors down), I overlook any excessive conviction close to to medium-term commerce right here.

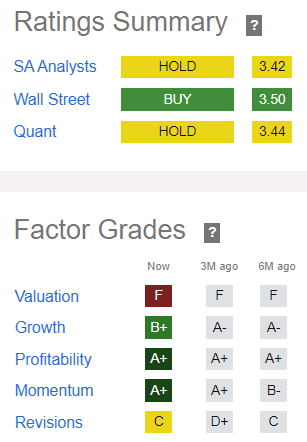

And SA’s Quant Score system agrees with this impartial stance:

TSLA Quant Rankings (Looking for Alpha)

During the last six months, Tesla’s “Momentum” issue grade has improved from “B- to A+” on the again of an epic rally within the inventory. Whereas TSLA’s “Profitability” issue grade has held up firmly at “A+” (regardless of margin deterioration), the weak point in monetary efficiency is driving “Progress” and (earnings) “Revisions” grades decrease. Total, Tesla is rated a ‘Maintain’ [3.44/5] by SA’s Quant Score system.

Given Tesla’s precarious technical setup and unsupportive quant issue grades, the near-term danger/reward for TSLA inventory is just not attractive sufficient for a brand new bullish place. Nevertheless, is Tesla a superb purchase from a long-term perspective? Let’s get a solution utilizing TQI’s Valuation Mannequin.

Is TSLA Inventory A Purchase, Promote, Or Maintain?

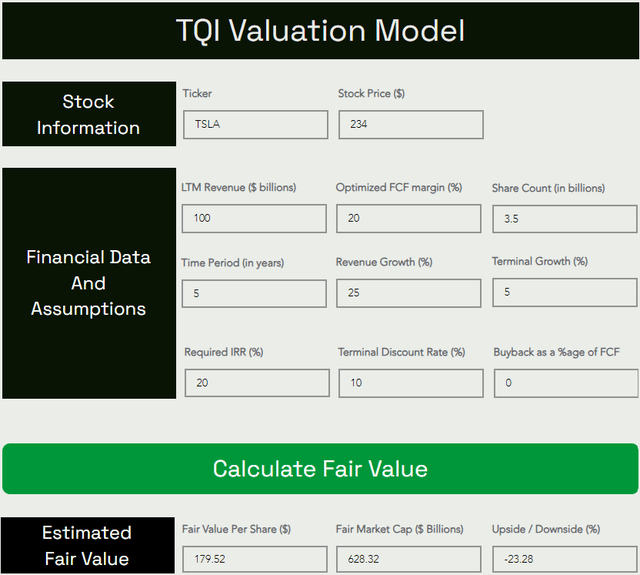

Regardless of Q3 2023 outcomes coming in decrease than avenue estimates, I’m sticking to my pre-earnings assumptions for Tesla. And as such, there is not any change to our honest worth estimate for the EV large.

Here is my up to date valuation for Tesla:

TQI Valuation Mannequin (TQIG.org)

In keeping with our mannequin, Tesla’s honest worth is ~$180 per share. With the inventory buying and selling at ~$234 per share (as of writing), it’s presently overvalued by ~23%. Now, I’m joyful to pay a premium for a high-quality firm like Tesla; nevertheless, is the chance/reward enticing sufficient to justify an funding at present ranges?

TQI Valuation Mannequin (TQIG.org)

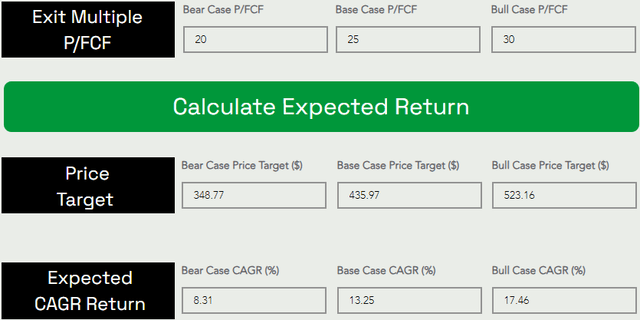

Assuming a base case P/FCF exit a number of of 25x, I see Tesla hitting $436 per share by 2027-28. As will be seen beneath, Tesla is projected to ship CAGR returns of 13.25% for the subsequent 5 years, which falls in need of my funding hurdle fee (min. required IRR) of 15%. From a long-term danger/reward perspective, I proceed to fee Tesla “Impartial/Maintain” at present ranges.

Concluding Ideas

With larger rates of interest (low affordability) the demand for brand spanking new autos is waning, and Tesla is clearly feeling the warmth, with income progress decelerating quickly and margins contracting considerably in Q3 2023.

As of at the moment, Tesla continues to be primarily an auto enterprise, and regardless of experiencing (self-inflicted) margin pressures, Tesla is on monitor to hit administration’s ~1.8M car gross sales goal for 2023. As Tesla’s factories in Berlin and Austin ramp as much as full manufacturing, margin pressures ought to ease off considerably. And newer merchandise like Tesla Semi and Cybertruck would probably permit additional scaling of Tesla’s auto enterprise in 2024.

A sub-$25K car is probably going wanted for Tesla to unlock the subsequent massive leg up in its auto market share, and as we all know, the corporate is already engaged on its next-gen platform to construct such a car. Tesla has already introduced a manufacturing unit in Mexico [delayed / slowed as of Q3 2023 until macro environment improves], and there is discuss of one other manufacturing unit to be built in India for a $24K automobile. Regardless of struggling margin compression, Tesla is rising its market share throughout geographies and increasing its fleet dimension at a brisk tempo in a difficult macroeconomic surroundings.

Total, Tesla Q3 2023 outcomes had been weaker-than-expected and the inventory is more likely to come below stress in upcoming days and weeks. Given Musk’s recession playbook of prioritizing car gross sales over profitability and the upcoming Cybertruck launch (and subsequent ramp), Tesla’s margins are more likely to keep below stress within the close to to medium time period. Now, regardless of going through margin compression, Tesla continues to be producing constructive free money circulation (“FCF”) and including to its rising money hoard of ~$26B, which ought to function a powerful basis for navigating by way of any financial downturn which will lie forward of us.

From a technical perspective, Tesla is primed for a big transfer in both route as value motion will get tighter in a triangle formation. From a valuation perspective, Tesla seems overvalued by ~25%, and at this level, TSLA is a binary guess on FSD.

In gentle of Q3 2023 earnings, my plan of motion for Tesla stays unchanged:

If we see a fast transfer to the $360-400 vary, I’ll e book partial income on my lengthy place.

Conversely, if we drop all the way down to $180, I’ll restart accumulation and add to my lengthy place.

Key Takeaway: I proceed to fee Tesla “Impartial/Maintain” within the $230s.

Thanks for studying, and joyful investing. When you’ve got any questions, ideas, and/or considerations, please share them within the feedback part beneath.