Authored by Simon Black, Bloomberg macro strategist,

The most recent cash information from China exhibits its capital-outflow downside is worsening, pressuring policymakers to permit an additional weakening within the foreign money.

China launched cash and inflation information over the weekend. CPI and PPI weren’t nice studying, however cash provide information was much more downbeat: M2’s progress dissatisfied, whereas M1 progress is moldering, falling 1.4% year-on-year versus +1.2% anticipated.

Actual M1 progress is now additionally contracting, which is ominous for China’s so far gingerly-improving progress.

China has a capital-outflow downside that’s placing strain on liquidity.

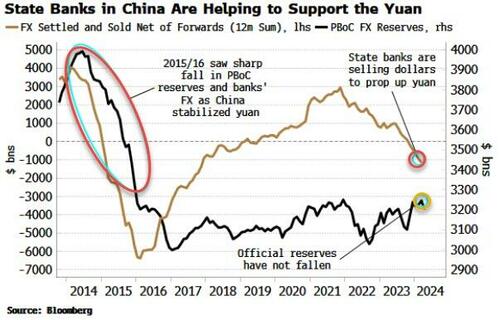

It has a nominally closed capital account, however we will infer capital outflow by wanting on the distinction between the commerce surplus and official reserves on the central financial institution, plus FX held at different banks.

Rising markets sometimes have overseas reserves forming their financial base because of the issue in reliably borrowing in their very own foreign money value effectively. When capital leaves a rustic that may comfortably borrow in its personal foreign money, the central financial institution can print cash to interchange the misplaced liquidity.

However in a rustic like China, capital outflow results in a mechanical fall in home liquidity.

Cuts within the required reserve ratio, with one other one anticipated subsequent month, and interest-rate reductions might help alleviate this decline. One other lever is the foreign money. A weaker yuan eases the strain on the autumn within the financial base as capital leaves.

USD/CNY continues to bump up towards the higher band of the yuan repair, signaling the strain the foreign money is beneath.

Overseas FX at banks is falling. A few of this probably as a result of capital outflow, however some can be as a result of China directing state banks to intervene to forestall the foreign money from weakening too far.

China continues to incrementally ease to attempt to kickstart a post-Covid traumatized financial system.

With a low debt-to-GDP ratio, the central authorities has scope to borrow extra. That’s taking place, with the Ministry of Finance right now saying it could difficulty the primary CNY 40 billion of ultra-long particular sovereign bonds of a complete of CNY 1 trillion between now and November.

Regardless of all this, the inventory market has been recovering a lot of the 12 months.

Oversold circumstances hinted a backside was close to.

Extra liquidity (actual cash progress minus financial progress) is supportive for the advance to proceed, as though actual cash progress is weak, so is financial progress, implying there’s sufficient “free” liquidity to search out its means into the market.

Loading…