sitox

I used to be a kind of individuals who have been skeptical about Nvidia Company’s (NASDAQ:NVDA) development potential because of the improve in geopolitical dangers. I additionally modified my thoughts just a few months in the past when the corporate aggressively elevated its steering simply as I used to be testing numerous generative AI apps to enhance my workflow effectivity.

Since Nvidia lately launched one other spectacular earnings report which indicated that the corporate’s development story is way from over, I are likely to imagine that it’s unlikely that its shares will enormously depreciate anytime quickly given all of the momentum that the enterprise has. On the identical time, there are additionally causes to imagine that regardless of having over $1 trillion in market cap, Nvidia’s inventory will not be actually overvalued and will recognize additional within the following quarters.

Nvidia’s Progress Story Is Not Over But

My newest article on Nvidia was printed simply earlier than the corporate launched its current earnings outcomes for Q2. I argued that it’s essential for the administration to as soon as once more overdeliver in order that the enterprise retains its momentum. That’s precisely what has occurred, as Nvidia’s revenues in Q2 elevated by 101.6% Y/Y to $13.51 billion and have been above expectations by $2.43 billion due to the surge in knowledge middle gross sales. On the identical time, the corporate’s non-GAAP EPS through the interval was $2.70, above the estimates by $0.61. Along with that, Nvidia as soon as once more shocked everybody by updating its outlook for Q3 the place it expects to generate $16 billion in revenues, above the consensus of $12.42 billion.

There are a number of causes to imagine that Nvidia may obtain that concentrate on. To start with, the generative AI trade is expected to develop at a CAGR of over 40% within the following decade, which already makes it doable for Nvidia to broaden its complete addressable market, or TAM, at an analogous price because the trade grows. On prime of that, there’s an indication that Nvidia’s flagship H100 GPUs will likely be bought out effectively into the following yr and the corporate is predicted to triple the output of its chips to as much as 2 million in 2024, up from round 500,000 models that the corporate is predicted to supply this yr. On the identical time, Nvidia’s foundry associate Taiwan Semiconductor (TSM) lately stated that the demand for Nvidia’s chips will persist for the following yr and a half, which provides causes for optimism in regards to the firm’s future.

What’s extra, is that earlier this month Nvidia has submitted its first benchmark outcomes for the upcoming Grace Hopper tremendous chip that’s going to be extra highly effective than H100 and is predicted to be launched in 2024. Along with that, there are causes to imagine that the corporate is working with TSMC on the silicon photonics tech to develop next-generation chips, and vital orders for them are anticipated to be positioned later in 2024.

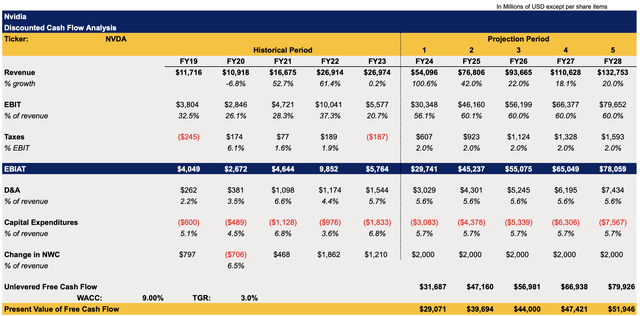

Contemplating all of this, it is sensible to imagine that Nvidia’s development story is way from over. Nonetheless, questions at the moment are being raised about whether or not the corporate’s inventory has an upside left as effectively because it already aggressively appreciated and now trades at over $1 trillion market cap. To reply these questions, I’ve made a brand new discounted money stream (“DCF”) mannequin that now could be extra carefully aligned with the newest Road forecasts which counsel that the corporate would proceed to develop at an aggressive price in years to come back.

The income and earnings assumptions within the mannequin are principally in-line with the Road estimates. The tax price is minimal, as Nvidia makes use of a number of offshore jurisdictions for tax optimization functions. All of the assumptions for different metrics within the mannequin are just like the corporate’s historic data. The WACC within the mannequin stands at 9% whereas the terminal development price is 3%.

Nvidia’s DCF Mannequin (Historic Knowledge: Searching for Alpha, Assumptions: Creator)

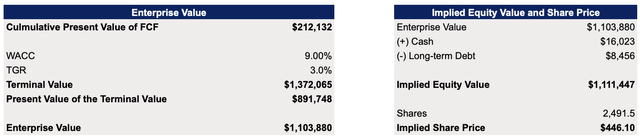

This DCF mannequin reveals that Nvidia’s honest worth is $446.10 per share, which is near the present market worth.

Nvidia’s DCF Mannequin (Historic Knowledge: Searching for Alpha, Assumptions: Creator)

Nonetheless, contemplating that the consensus on the Road is that Nvidia’s honest worth is over $600 per share, it’s doable that the upside may very well be higher than I at present estimate. Add to all of this the truth that tech corporations nearly at all times commerce at a major premium, and we may assume that my DCF may very well be too conservative given the forecasted aggressive development of the general generative AI trade within the following years.

A number of Dangers To Think about

Regardless of these development catalysts described above, it’s vital to know {that a} weaker development of the general world financial system may however lead to a weaker development of Nvidia’s gross sales. Whereas it’s unlikely to be the case now, as numerous reports point out that the corporate sells its superior GPUs at a 1000% revenue margin, the macro challenges may undermine Nvidia’s development story within the long-term.

On prime of that, despite the fact that the geopolitical dangers decreased since final October when the Biden administration introduced new export restrictions on superior chips to China, it might nonetheless be too naive to assume that such dangers gained’t return sooner or later. Final month, the U.S. has already expanded the export restrictions to a number of nations within the Center East. On the identical time, Nvidia lately warned that additional restrictions may harm American corporations, as its personal knowledge middle gross sales to China account for 20% to 25% of the general knowledge middle gross sales. As such, potential additional restrictions would definitely negatively have an effect on Nvidia’s efficiency and will undermine the bullish thesis.

The Backside Line

Regardless of all the macro and geopolitical dangers, the newest gross sales knowledge together with the improved steering level to the truth that Nvidia Company’s development story is way from over and its inventory has extra room for development. Whereas the corporate’s shares lately barely depreciated together with the remainder of the market, I anticipate them to rebound within the foreseeable future as they’ve a powerful technical help degree of round $400 per share whereas the general enterprise nonetheless has momentum going for it. As such, I’m planning on opening an extended place within the firm quickly and can doubtless maintain it for the long-term since there are causes to imagine that Nvidia will proceed to energy the present generative AI revolution for years to come back.

Nvidia’s Inventory Efficiency (Searching for Alpha)

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please pay attention to the dangers related to these shares.