Spencer Platt/Getty Photographs Information

Just a few months in the past, we wrote an article titled “The Prime 3 Causes To Purchase CVS Well being”.

The article targeted on the highest parts of our bull thesis on CVS (NYSE:CVS), together with the resilient financials, spectacular scale, and enticing valuation.

Because it at present stands, the inventory is up greater than 14% since this preliminary article, greater than double the return of the S&P 500 over that timeframe.

That stated, we predict the corporate stays a compelling purchase.

The corporate’s earnings in November of 2023 re-affirmed our thesis, and the valuation, at solely 12x GAAP P/E, makes the corporate probably the most attractively valued shares in the marketplace.

As we speak, we’ll break down what has occurred with CVS since we final printed on the corporate, and clarify why we’re retaining our “Purchase” score on the inventory – regardless of the latest run-up in share worth.

Our Thesis

In case you missed our preliminary article, our “Purchase” thesis on CVS relies on three issues: the financials, the moat, and the valuation. Here is a abstract of the case we made in September:

-

Robust Monetary Efficiency:

- CVS Well being has demonstrated strong monetary efficiency regardless of its inventory dip in 2023.

- Shareholders have witnessed steady beats in each high and bottom-line expectations for greater than 5 years, with latest quarterly income reaching $89 billion (10% YoY development).

- Earnings and FCF have persistently elevated, highlighting robust money conversion and well-run operations, distinguishing CVS from retail rivals like Walgreens (WBA) and Ceremony Support (OTC:RADCQ).

-

Huge Scale and Built-in Choices:

- CVS’s merger with Aetna in late 2018 positioned it as the primary totally built-in healthcare firm at scale within the U.S.

- The corporate operates via three revenue-producing segments: Pharmacy Companies, Well being Companies, and Well being Care Advantages, offering a complete healthcare product to greater than 100 million prospects.

- CVS’s scale permits for cross-selling alternatives throughout totally different dimensions of human well being, resulting in robust income and revenue diversification.

-

Enticing Valuation:

- CVS at present trades at a beautiful valuation; 0.27x gross sales and 5.16x free money move. This represents 5-year lows and a traditionally advantageous entry level.

- The valuation seems to be a fantastic deal primarily based on historic values and is supported by a “B+” worth rating from Searching for Alpha’s Quant Score System.

- The inventory additionally sports activities a stable 3.4% dividend yield.

What’s Modified?

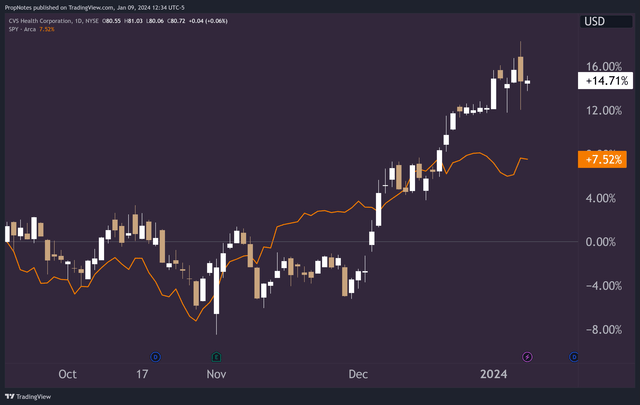

Since our article, the inventory went on a 14% run, beating the S&P 500’s complete return:

TradingView

A few of this rally was possible because of the firm’s Q3 earnings report, which confirmed continued development and resilience in what stays a aggressive general setting.

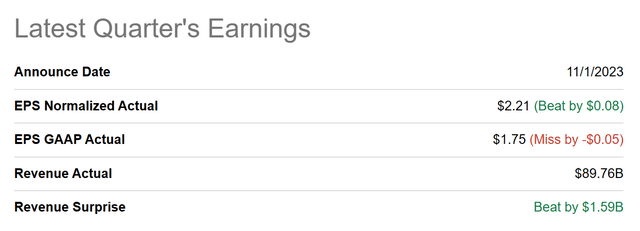

Regardless of the GAAP EPS miss, the Q3 normalized EPS and income numbers each beat, which continues the corporate’s robust monitor document of continued high and bottom-line beats:

Searching for Alpha

Along with the monetary beats, administration retains a optimistic outlook for the enterprise on a go-forward foundation:

We generated excellent working money flows, bringing our year-to-date complete to $16.1 billion. We’re reconfirming our steering vary for 2023 adjusted EPS of $8.50 to $8.70, this displays execution in opposition to our technique with robust efficiency in our Pharmacy & Shopper Wellness phase and continued momentum in our Well being Companies phase, offsetting incremental Medicare Benefit medical value pressures in our Well being Care Advantages phase.

This quote from CEO Karen Lynch additionally highlights one of many firm’s different strengths; the robust income range.

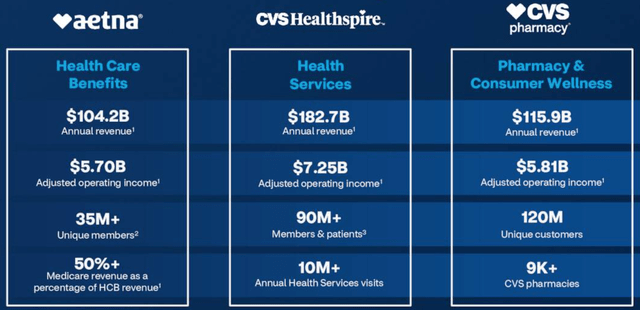

Of their latest presentation on the JP Morgan Healthcare convention in San Francisco, CVS re-iterated the power in its 3-pronged method to healthcare:

CVS Presentation

As every of those three prongs are comparable in working earnings dimension, the enterprise is of course hedged in opposition to fluctuations within the healthcare market, which provides the corporate the flexibleness to give attention to growing EPS over the long run.

Fortunately, that is precisely the place administration is concentrated:

CVS Presentation

Proper now, the corporate sees future enhancements to Medicare benefit margins, which ought to add to an already spectacular ground of 6% EPS development over the interim.

Different development vectors embrace Cordavis, a brand new (totally owned) biosimilar producer and distribution firm. This new subsidiary, launched in August of 2023, ought to present higher costs to CVS prospects on widespread drugs, additional enhancing CVS’s pharmacy enterprise & value construction.

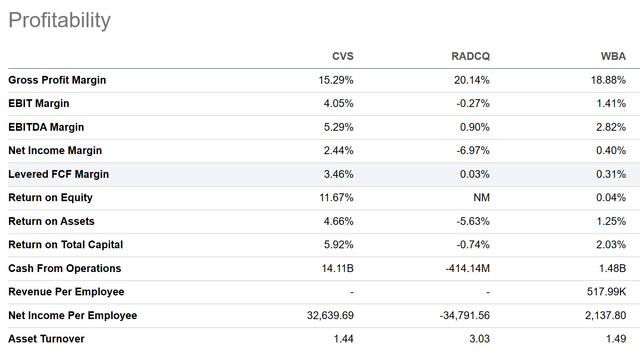

When put next with Ceremony Support and Walgreens, it is clear that the merger with Aetna in 2018 was the proper transfer on the subject of the aggressive setting, and thus profitability & return on fairness:

Searching for Alpha

Lastly, liquidity is in a great place, with web debt at $63 billion, annual free money move of $13 billion, and no near-term cliffs or maturities.

Taken collectively, CVS continues to develop and produce robust monetary outcomes as a consequence of its robust market place and moat inside the U.S. healthcare trade.

The Valuation

Regardless of administration’s continued execution throughout the board as outlined, CVS’s inventory stays properly priced.

If the corporate hits their FY23 EPS goal of $8.50-$8.70, CVS can be buying and selling at roughly 9.3x web earnings in 30 days’ time. When taking administration’s steering into consideration with the corporate’s monitor document, we predict that $8.50-$8.70 is totally achievable.

It is a nice deal, each nominally and traditionally.

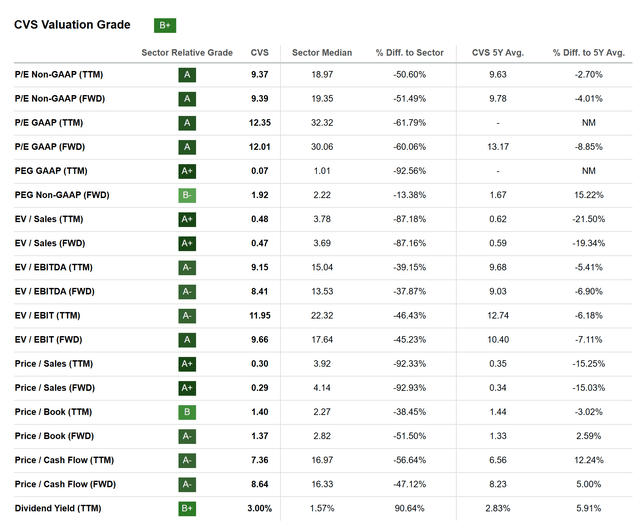

From a historic perspective, CVS is buying and selling at an 8-12% low cost to the place it has traditionally over the past 5 years. This extends to a greater than ~20% low cost in some circumstances, just like the EV/Gross sales a number of:

Searching for Alpha

The Searching for Alpha Quant Score System additionally assigns the corporate a score of “B+”, which signifies that the corporate is properly priced vs. its sector.

This features a 60% decrease P/E than different healthcare corporations.

Whereas that is possible skewed because of the variety of high-multiple drug corporations which can be creating promising new medicine and therapies, the low cost right here actually stands out.

Lastly, CVS’s potential 9.3x web earnings a number of stands in distinction to the S&P 500’s ~25x backside line valuation, even supposing CVS has an in-line future development trajectory.

All in all, the corporate is attractively priced, even when bearing in mind the latest run-up in shares. It will take a rally in the direction of ~$140 for the corporate to be extra totally valued, in our eyes.

Dangers

There are some dangers to purchasing CVS presently, together with additional deterioration in Medicare margins, which, to a point, are on the mercy of prevailing politics.

Aside from that, although, CVS seems properly insulated from many, many dangers as an organization – this is without doubt one of the major the explanation why we prefer it a lot from a long-term standpoint. The valuation is already discounted and enticing, the enterprise is self-hedging, and the demand for healthcare is not going anyplace.

Maybe in the long run, demographic shifts round fertility charges and slowing inhabitants development (and even decline) would offer some earnings headwinds to CVS.

Moreover, it is doable that different healthcare supply strategies sooner or later might disrupt CVS; both digitally, or by way of a brand new pricing mannequin.

Nevertheless, in the meanwhile, issues seem like buzzing alongside. And, given any developments on the above subjects, we predict the corporate, with almost 350 billion in income, is able to act and shield itself.

Abstract

In sum, CVS stays a beautiful long-term funding resulting from its robust outcomes, spectacular scale, and enticing valuation.

The latest rally in shares following our first article should not dissuade any new entrants from shopping for, or induce present traders to promote. There’s nonetheless a protracted runway for fulfillment right here as an investor, whether or not it is via the dividend, a number of growth, or continued administration execution.

We re-iterate our score of CVS as a “Purchase”.