photoschmidt

We beforehand mentioned Bristol-Myers Squibb Firm (NYSE:BMY) in September 2023, discussing its Loss Of Exclusivity difficulty with its main product, Revlimid, resulting in a major decline in annualized gross sales to $5.5B in 2023, in comparison with $12.82B in 2021.

Mixed with the shortcoming of its different pipelines to offset the losses within the close to time period, we had most well-liked to price the inventory as a Maintain then.

On this article, we will talk about why our earlier Maintain ranking has confirmed to be prudent, with the BMY inventory dropping -12.35% of its worth since then.

Whereas the inventory has bounced reasonably by early December 2023, we aren’t sure if this backside could maintain, attributed to potential steadiness sheet deterioration after the all-cash $4.8B Mirati deal (MRTX) is closed by someday in H1’24.

Whereas the pharmaceutical firm’s profitability metrics have been enhancing past expectations, we preserve our Maintain ranking, since it’s unsure if the latest M&A actions could bear fruit forward.

BMY’s Dividend Funding Thesis Seems To Be Sound

For now, BMY has reported a backside line beat in its FQ3’23 earnings name, with revenues of $10.96B (-2.3% QoQ/ -2.2% YoY) and adj EPS of $2.00 (+14.2% QoQ/ +0.5% YoY). That is a powerful feat certainly, with Revlimid’s top-line erosion of $1.42B (-2.7% QoQ/ -41.3% YoY) showing to be decelerating as properly.

Most significantly, its two different top-line drivers, Opdivo has delivered a wonderful gross sales development of $2.27B (+6% QoQ/ +11.2% YoY), as with Eliquis at $2.7B (-15.6% QoQ/ +1.8% YoY), partly balancing Revlimid’s decline to this point.

The BMY administration has additionally made nice efforts to enhance its gross margins to 77.3% by the newest quarter (+2.3 factors QoQ/ -2.5 YoY), up drastically from 69.8% in FY2019 (-1.8 factors YoY) and 72.3% in FY2020 (+2.5 factors YoY).

As well as, the administration has optimized its working bills to an annualized sum of $25.48B (-0.7% QoQ/ -2.4% YoY), down from $27.35B in FY2020 (+124.7% YoY, although non-comparable because of the Celgene acquisition in November 2019).

A lot of the tailwinds are additionally attributed to BMY’s sustained debt reimbursement, with FQ3’23 bringing forth decrease long-term money owed of $32.19B (-7.1% QoQ/ -13.2% YoY/ -33.4% from its peak money owed of $48.34B in FY2020).

This has naturally contributed to its moderating annualized internet curiosity bills of $796M (+6.4% QoQ/ -19.4% YoY/ -36.8% from FY2020), naturally boosting its backside line.

Because of this, it’s unsurprising that BMY’s dividend funding thesis stays strong, with a powerful Money From Operations of $12.91B (-6.4% sequentially) and Free Money Circulation of $11.68B (-8.1% sequentially) over the LTM.

This means a greater than first rate FCF margin of 26% (-1.2 factors sequentially) in comparison with its pre-pandemic averages of 25% and hyper-pandemic averages of 30%.

That is on prime of BMY’s constant share repurchases over the previous few years, with the pharmaceutical firm reporting 2.064B of shares excellent by the newest quarter (-38M QoQ/ -84M YoY/ -194M from FY2020).

The decreased share rely has straight allowed the administration to sustainably develop its dividend per share at a CAGR of +8.20% over the previous three years as properly.

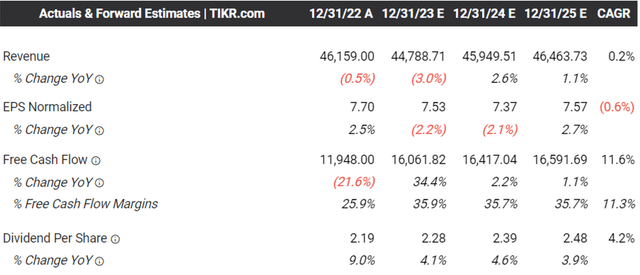

The Consensus Ahead Estimates

Tikr Terminal

On the one hand, the consensus estimates that BMY could generate an impacted prime and backside line development at a CAGR of +0.2% and -0.6% by way of FY2025, in comparison with its historic development at a CAGR of +15.5% and +18.2% between FY2016 and FY2022, respectively.

Alternatively, the pharmaceutical firm’s most necessary side, which is its Free Money Circulation technology, are anticipated to enhance significantly shifting ahead.

As mentioned above, the BMY administration’s laser give attention to revenue enlargement has proven nice outcomes to this point, with the consensus already estimating a median of FCF margin of over 35% over the following few years.

Mixed with the just lately raised annualized dividend to $2.40 (+5.35%), we are able to perceive why the In search of Alpha Quant continues to price its Dividend Security as a B+, regardless of Revlimid’s Loss Of Exclusivity points to this point.

That is made engaging by BMY’s depressed inventory costs, naturally triggering its expanded ahead dividend yield of 4.61% in comparison with the sector median of 1.58% and 4Y historic common of three.09%.

Nevertheless, It Stays To Be Seen If BMY’s M&A Actions Could Generate A Profitable Pipeline

BMY has tried to bolster its pipeline by way of a number of partnerships and acquisitions over the previous few months, specifically the Mirati Therapeutics (MRTX) all-cash acquisition price $4.8B and partnership with SystImmune price as much as $8.4B in staged funds.

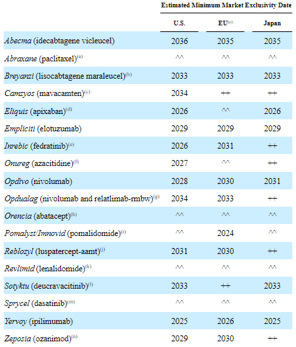

BMY’s Upcoming Loss Of Exclusivity

In search of Alpha

That is naturally to steadiness BMY’s upcoming LOEs for Eliquis and Inrebic by 2026 within the US, price an annualized income of $10.93B in FQ3’23 (-15.4% QoQ/ +2.1% YoY).

Based mostly on its deteriorating internet money place, it’s unsurprising that the administration has priced a $4.5B of senior unsecured notes to fund the MRTX acquisition, although with a comparatively properly laddered maturity of between 2031 and 2063.

Whereas SystImmune’s BL-B01D1 is probably a first-in-class bispecific EGFRxHER3 ADC for the remedy of lung and breast cancer, with a projected TAM of $86.5B and $73.68B by 2032, respectively, the candidate is simply in Phase 1 clinical trials with it remaining to be seen when and if the US FDA approval could also be obtained.

With solely ~8% of clinical trials having the ability to obtain the coveted regulatory approval, BMY’s upfront/ near-term funds of $1.3B to SystImmune seems to be hefty certainly, with the BL-B01D1 improvement prone to be extended over the following few years.

Which means we may even see the pharmaceutical firm’s steadiness sheet reverse its latest positive aspects, with the pharmaceutical firm prone to face reasonable headwinds in profitability within the close to time period.

Readers should additionally observe that BMY faces $6.7B of debt maturity by way of 2026, with one other $3.2B in curiosity obligations on the similar time.

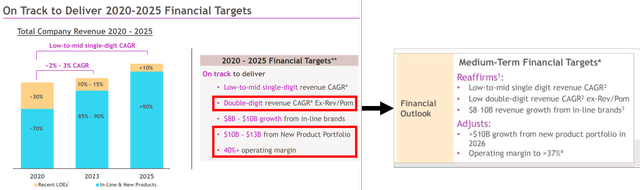

BMY’s 2025 Monetary Goal

BMY

Whereas BMY continues to reaffirm its medium term guidance to a big extent, traders should additionally observe that some numbers have been reasonably downgraded.

This features a decrease double-digit development in its Ex-Income phase, extended >$10B gross sales from its New Product Portfolio from 2025 to 2026, and lowered working margin from 40% to 37%.

Whereas that is partly attributed to the unprofitable MRTX, it’s obvious that we may even see BMY’s FCF technology reasonably impacted within the intermediate time period, worsened by the elevated debt reliance and curiosity bills.

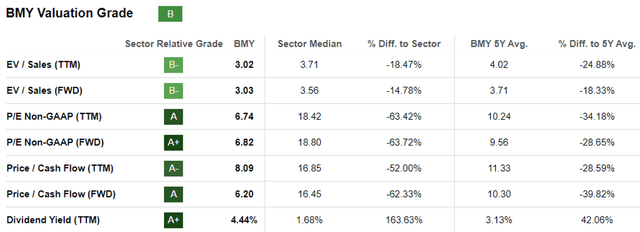

BMY Valuations

In search of Alpha

Maybe that is why BMY’s FWD P/E valuation of 6.82x and FWD Value/ Money Circulation of 6.20x have been drastically impacted in comparison with their 1Y imply of 8.05x/ 9.26x, 3Y pre-pandemic imply of 15.78x/ 18.22x, and sector median of 18.80x/ 16.45x, respectively.

Based mostly on the stagnant projected EPS development over the following few years, it seems that BMY could at greatest commerce sideways from present ranges, till a breakthrough is achieved and a extremely worthwhile remedy is discovered, akin to Novo Nordisk’s (NVO) and Eli Lilly’s (LLY) GLP-1 medication.

So, Is BMY Inventory A Purchase, Promote, or Maintain?

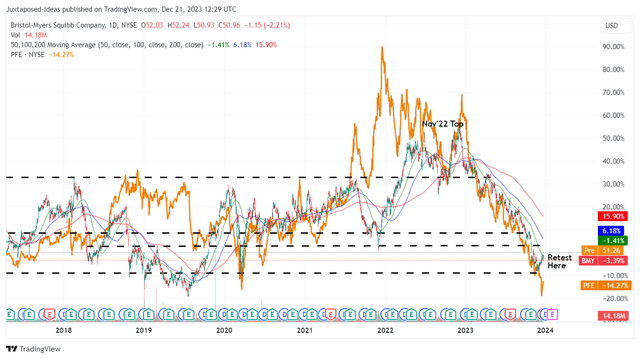

BMY 5Y Inventory Value

Buying and selling View

For now, BMY has fallen drastically by -34.9% since its November 2022 prime, with it showing to search out bullish help on the $48s.

Based mostly on its historic worth chart over the previous few years, it is usually obvious that many traders could have been within the pink, with the one comfort being its 7Y consecutive years of dividend development.

With Pfizer (PFE) on a equally miserable boat, we consider that BMY’s dividend funding thesis will not be appropriate for everybody, particularly when evaluating the latter’s ahead dividend yield of 4.61% and the US Treasury 3M/ 6M Yields of 5.37%/ 5.30%.

Mixed with the speculative nature of its pipeline and the extended monetary goal by way of 2026, we want to proceed ranking the BMY inventory as a Maintain (Impartial) right here, since it’s unsure when the correction could finish and if the ground could maintain at $48s.

Persistence could also be extra prudent right here.