Written by Nick Ackerman, co-produced by Stanford Chemist.

abrdn International Infrastructure Revenue Fund (NYSE:ASGI) is uniquely positioned the place the fund has overweighted industrial shares. This had deviated from the normal infrastructure closed-end funds that always allocate their portfolios to utilities and power infrastructure investments. That positioning has helped the fund this yr relative to different infrastructure friends.

Not solely did its differentiated positioning assist, however the truth that the fund additionally is not incorporating leverage on the fund degree is one other plus on this rising price setting. The deep low cost on an absolute foundation relative to friends and even all CEFs can create a longer-term alternative as effectively.

The Fundamentals

1-Yr Z-score: -2.48

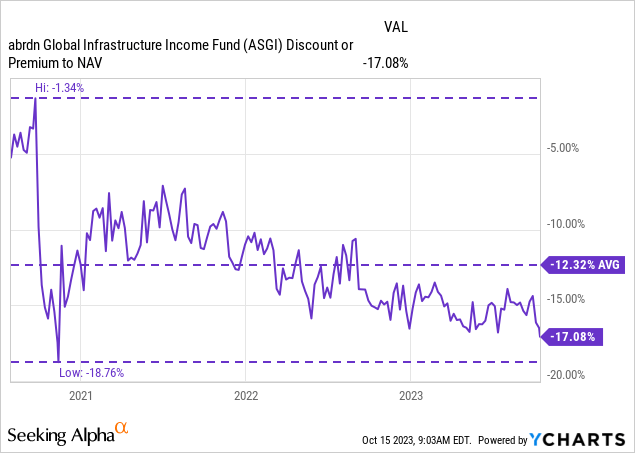

Low cost: -17.08%

Distribution Yield: 9.59%

Expense Ratio: 1.75%

Leverage: N/A

Managed Property: $544 million

Construction: Time period (anticipated liquidation date round July 28, 2035)

ASGI’s investment objective is “to search to supply a excessive degree of whole return with an emphasis on present earnings.”

To attain this goal, the funding technique is sort of easy. They are going to “put money into a portfolio of income-producing private and non-private infrastructure fairness investments from around the globe.” Apparently, probably the most vital publicity in ASGI is to industrial shares, making this fund a bit distinctive within the infrastructure house. Nonetheless, utilities are proper up there when it comes to publicity.

ASGI not using leverage on the fund has been one of many primary promoting factors of this fund, in my view. Nonetheless, the low cost relative to its older friends would point out that the sentiment is not shared extra broadly. With no leverage, the fund could possibly be thought-about comparatively extra conservative because it takes away an added layer of probably making the fund extra unstable. Moreover, with rising rates of interest, most funds are actually paying over 6% for his or her borrowings, which is one thing ASGI buyers do not have to think about on the fund degree.

The fund’s expense ratio was last reported at 1.75%; nonetheless, because of the merger we mentioned beforehand, that will probably be capped at 1.65% for the following yr. The cap is constructive, however ultimately, that is nonetheless one of many highest expense ratios for a non-leveraged fund, which is an total adverse. One of many arguments for the justification of this larger expense ratio is that the fund additionally intends to put money into personal investments, which takes a bit extra work.

After changing into a bigger fund earlier this yr, the fund is about to grow to be even bigger once more. Macquarie/First Belief International Infrastructure/Utilities Dividend & Revenue Fund (MFD) is set to be merged with ASGI. That is anticipated to happen in February 2024. In fact, topic to the approval of MFD shareholders.

MFD is a a lot smaller fund than Macquarie International Infrastructure Complete Return Fund (MGU). MGU had practically double the online belongings that ASGI did, which made ASGI considerably bigger on a relative foundation. Nonetheless, even the ~$70 million in web belongings that MFD would deliver would make ASGI a bigger fund. And a bigger fund means doubtlessly extra liquidity for shareholders.

Comparatively Robust Efficiency And Deep Low cost Current Alternative

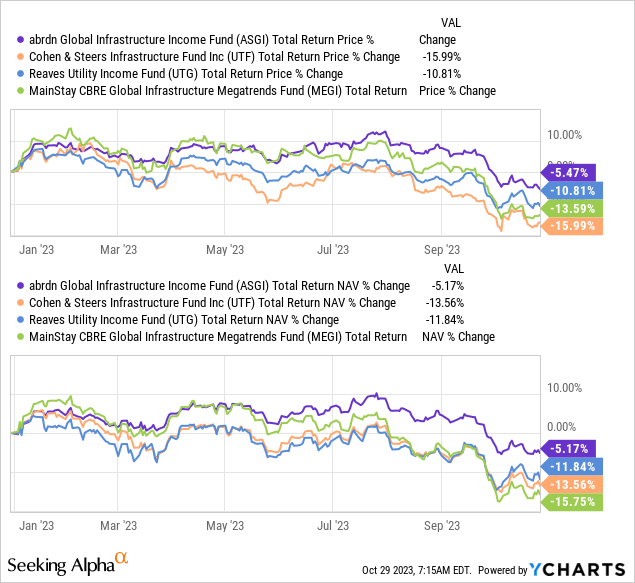

Right here is the YTD efficiency on a complete share value and NAV return foundation of ASGI relative to some friends. These friends embrace the extra in style Cohen & Steers Infrastructure Fund (UTF) and Reaves Utility Revenue Fund (UTG). I’ve additionally included the MainStay CBRE International Infrastructure Megatrends Fund (MEGI) – which I additionally imagine has some attraction, and I seemed on the final time when taking a look at ASGI as effectively.

MEGI is one other infrastructure fund that strays from the extra conventional asset allocation of what one would anticipate within the infrastructure CEF house. Nonetheless, that differentiated strategy has not yielded any advantages by means of this time period because it was the worst acting on a complete NAV return foundation. Nonetheless, MEGI is an attention-grabbing fund. MEGI and ASGI are the newer infrastructure funds relative to UTF and UTG. MEGI is price exploring additional in one other future replace.

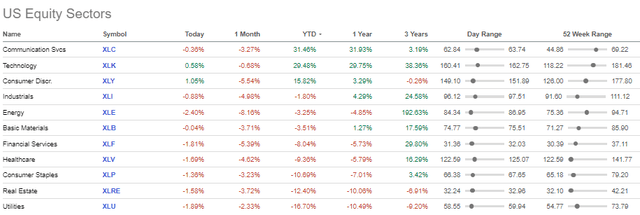

With that being stated, the primary fund we’re discussing at the moment is ASGI, and we will see that it has carried out the most effective on a YTD foundation. As utilities have been slammed up to now this yr, being the worst performing sector by far, that is the place the differentiated positioning and no leverage of the fund actually shined by means of.

Whereas industrials aren’t essentially blowing it away when it comes to efficiency, coming in primarily flat on a YTD foundation, they’re nonetheless within the high half of sectors on a YTD foundation. At this level, the utility sector is down nearly 17% as larger rates of interest have put vital strain on that space of the market in additional methods than one.

U.S. Sector Efficiency (In search of Alpha)

One other issue that buyers may take into account is the valuation of ASGI at present. The fund rapidly went to a pointy low cost, as most CEFs do after launching. Whereas we aren’t precisely on the new lows when it comes to the fund low cost, this nonetheless represents a time when the fund is buying and selling at one of many deepest reductions since its launch a number of years in the past.

Ycharts

This could possibly be one thing to proceed to observe over the approaching years, being a time period fund. Although, on this case, the fund’s anticipated liquidation date is not till 2035, so we undoubtedly have a while earlier than that turns into a consider making use of any sway for the fund.

Interesting And Affordable Distribution

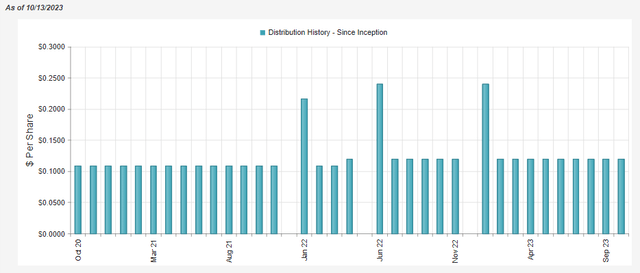

The fund launched with a $0.1083 month-to-month distribution and bumped it as much as $0.12 in 2022.

ASGI Distribution Historical past (CEFConnect)

Apart from shopping for belongings at a deep low cost with this fund, one other attribute of deeply discounted funds is the ‘enhanced’ distribution that buyers obtain. On this case, the fund’s distribution yield involves 9.59%, whereas the fund’s NAV price involves a extra modest 7.90%. At that NAV price, I imagine that is an inexpensive payout degree that they need to be capable to keep for the foreseeable future.

On the very least, it’s placing it in a a lot better place relative to its older friends UTF and UTG, the place they’re paying related distribution charges at present however with shallow reductions means their portfolios need to generate nearly the identical return going ahead for them to be coated. That leaves ASGI rather more versatile with a low distribution price.

Then again, all of those funds, being fairness funds, will rely considerably on capital positive factors to fund their payouts. The underlying holdings they’re invested in do not pay these 9%+ charges (and even 7.7%+ charges within the case of ASGI.) Subsequently, they are going to require appreciation going ahead sooner or later so as to justify paying these present charges. Both that, or the fund will erode away, and the NAV charges will simply creep larger and better till they’re ready the place they should minimize the payouts.

ASGI’s web funding earnings protection is available in at simply 6.25%. That is additionally a operate of the fund’s underlying holdings, however a better working expense ratio retains NII decrease.

ASGI Semi-Annual Report (abrdn)

Here’s a take a look at the distribution tax classifications that we mentioned beforehand:

As is mostly the case with fairness funds, a big part of the distribution was categorized as long-term capital positive factors. That is according to the earnings we noticed above, however all the time a great reminder that it’s not all the time the case. Generally earnings and distribution classifications can differ wildly.

In 2022 this was mirrored, however 2021 confirmed largely extraordinary earnings because the fund was getting began. Holding this fund in a taxable account could possibly be applicable as long-term capital achieve distributions are tax-friendly in comparison with extraordinary earnings.

ASGI Distribution Tax Classification (abrdn)

ASGI’s Portfolio

As regards to decrease NII, a number of the fund’s positions do not pay any dividends in any respect. A number of of the holdings exterior the U.S. that additionally make up the most important holdings within the fund pay semi-annual dividends based mostly on earnings. That is totally different from most U.S. firms that always attempt to goal quarterly dividends that develop over time.

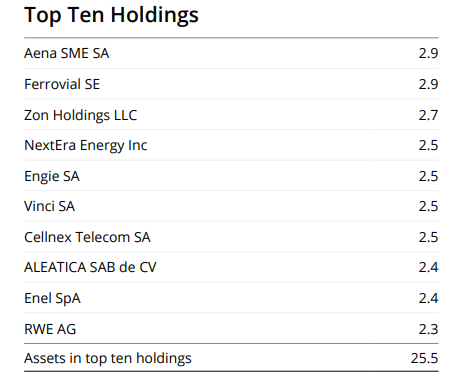

ASGI Prime Ten Holdings (abrdn)

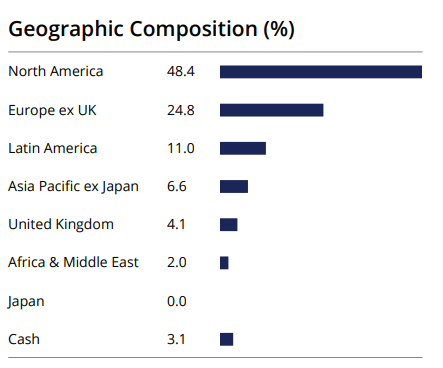

The fund’s high ten positions are largely positioned exterior the U.S. Nonetheless, the fund nonetheless lists practically 50% of the portfolio is invested in North American corporations.

ASGI Geographic Publicity (abrdn)

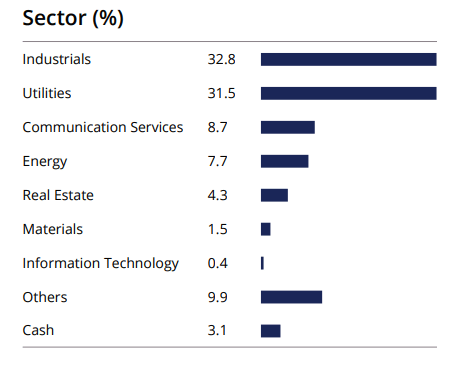

The fund’s weighting to industrials has ceaselessly been the fund’s largest sector allocation. In reality, from earlier this yr, the fund has seen its industrial publicity improve, in addition to the fund’s utility weighting, has grown a contact, too.

ASGI Sector Allocation (abrdn)

The fund’s largest holding, Aena S.M.E., S.A. (OTCPK:ANYYY), is an instance of an industrial sector firm that operates within the airport providers business. The corporate is headquartered in Spain and has operations in Spain, Brazil, the U.Ok., Mexico and Columbia. An instance of an organization that’s an industrial inventory however is oriented towards infrastructure because it gives a service for the general public.

Ferrovial SE (OTCPK:FRRVY) is one other place that reveals up as a high ten place and is one other Spanish firm within the industrial sector. Nonetheless, the business right here is labeled as “building and engineering.” The company defines a number of enterprise traces that they’re concerned with: highways, airports, building, power infrastructure, mobility and “different enterprise.”

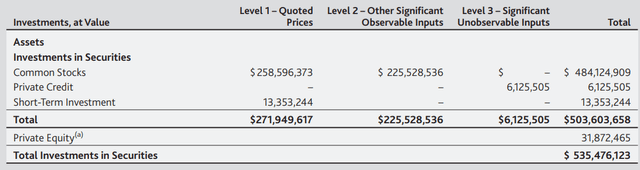

The fund’s personal holdings are one motive that some low cost is probably going warranted. Non-public investments add some uncertainty to the valuation. As of their final holdings listing for the interval ending June 30, 2023, personal holdings have been as much as round 7.7%. That is not essentially the most important quantity, and we had truly seen that not all of their personal holdings are thought-about degree 3 securities. Degree 3 securities have been solely round 1.15% of the fund beforehand as of their final semi-annual report.

ASGI Degree of Safety (abrdn)

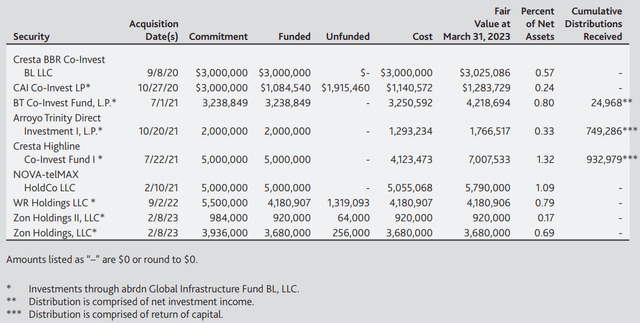

Listed below are the personal holdings listed with their prices and honest market worth. A number of the holdings are newer investments that have not seen their values change but.

ASGI Non-public Holdings (abrdn)

Virtually all of their personal holdings are held by means of abrdn International Infrastructure Fund BL, LLC. This automobile is then owned by ASGI and is consolidated into the fund’s operations.

Nonetheless, this additionally highlights that months can go by with none adjustments in any respect to the valuations. The valuations aren’t often modified till a brand new spherical of funding goes by means of, and through situations comparable to a tricky market, some funding is not carried out for an extended whereas. These have been the valuations as of their final semi-annual report.

Non-public funding publicity has ticked up since then, however it would not have been sufficient to actually make a significant distinction from earlier this yr. Subsequently, I believe the valuation of the portfolio in all fairness correct for probably the most half, with the majority of the portfolio in degree 1 or 2 classifications exterior of the 7.7% personal holdings weight. Zon Holdings is the fund’s third-largest place as of the final replace, is an instance of one among their personal funding.

Conclusion

UTF and UTG are each strong funds, however they’re definitely in a special state of affairs in the meanwhile in comparison with ASGI. Whereas I would not advocate for one over the opposite, I imagine that ASGI is price taking a look at for some infrastructure publicity. We already noticed how the differentiated strategy of the portfolio can lead to totally different efficiency, which I imagine helps justify holding a mixture of the funds as an alternative of getting to decide on one over one other.

There are definitely short-term headwinds that would strain this fund’s underlying holdings going ahead, comparable to a slowdown within the world economic system. Nonetheless, for long-term buyers, I imagine it nonetheless presents a pretty alternative to take a position on this fund whereas it’s at a deep low cost.