Liudmila Chernetska

We beforehand lined Altria (NYSE:MO) in August 2023, discussing its dedication to rebuild its various tobacco phase after the Juul fiasco, attributed to the just lately introduced NJOY acquisition.

We had cautiously rated the inventory as a Purchase then, because of its sturdy profitability and tempting dividends, whereas warning traders to watch its progress within the Smokeable Product phase, as a result of sustained decline in gross sales quantity.

On this article, we can be discussing MO’s sturdy dividend funding thesis, regardless of the repeatedly deteriorating gross sales volumes for Smokeable Product, as a result of rising demand for Vapour Pods and Heated Tobacco Sticks globally.

Whereas the tobacco firm’s progress within the various tobacco phase has been slower than its opponents, we’re keen to patiently watch for its eventual reversal, with NJOY prone to speed up in gross sales/ market share achieve by H1’24.

The Standard Tobacco Funding Thesis Continues To Deteriorate

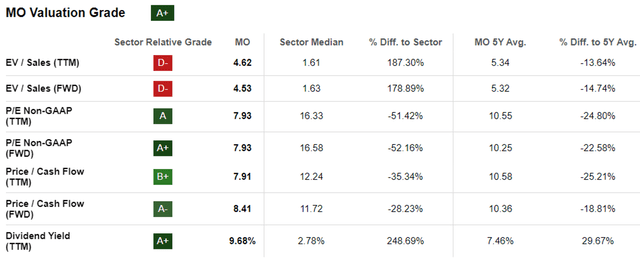

MO Valuations

In search of Alpha

Because of the current sell-off, MO’s FWD valuations have been moderated in comparison with its 5Y averages and sector medians.

On the one hand, we consider that the correction has been overly accomplished, because the administration has solely narrowed its FY2023 adj EPS steerage from the earlier vary of between $4.89 – $5.03 to $4.91 – $4.99, implying a minimal influence of $0.01 on the midpoint.

With the up to date vary nonetheless representing a +2.2% development YoY, in comparison with the earlier +2.4%, we’re not overly involved.

Then again, we consider that a lot of the pessimism embedded in MO’s valuations is the sustained decline in its Smokeable Product volumes of 19.75B (-6% QoQ/ -11.3% YoY) by the most recent quarter.

Most notably, the demand for Marlboro merchandise seem to have moderated to a gross sales quantity of 17.43B (-5.7% QoQ/ -10.5% YoY). Whereas the model’s retail share appears to be steady at 42.3% (+0.2 factors QoQ/ -0.3 YoY), it’s obvious that the present clients’ model loyalty has not been sufficient to stave off the gross sales headwinds.

Since MO’s Smokeable Product phase includes $5.57B (-4.2% QoQ/ -5.2% YoY) and $2.74B (-3.5% QoQ/ -1.7% YoY) of its general high and backside traces of $6.28B (-3.3% QoQ/ -4.1% YoY) and $3.08B (+6.2% QoQ/ -1% YoY) within the newest quarter, respectively, it’s unsurprising Mr. Market is more and more involved.

There could also be a restrict to its worth hikes in addition to the macroeconomic outlook stays unsure, because the +$420M tailwinds from the raised costs has not been capable of offset the decrease cargo quantity headwinds of -$725M within the newest quarter.

The identical has been reported in its first 9 months efficiency, with the decrease cargo quantity (-$1.92B) solely partially offset by the upper pricing (+$1.38B).

MO’s Dividend Funding Thesis Stays Strong

Then once more, we consider that MO’s dividends stay secure, based mostly on its Web money supplied by (utilized in) working actions of $6.06B over the previous three quarters (+7.6% YoY) and quarterly dividend payout of roughly $1.6B.

Because of this its TTM Free Money Circulation Yield to Dividend Yield Ratio has reasonably improved to 1.41% in comparison with its 5Y common of 1.29%, although nonetheless lagging behind the sector median of 1.63%.

MO has additionally been constantly deleveraging its steadiness sheet, with a long-term money owed of $23.97B (-0.4% QoQ/ -3.5% YoY) by the most recent quarter, down from its FY2019 ranges of $27.04B (+127.4% YoY).

Regardless of the influence of the elevated rate of interest surroundings to its annualized FQ3’23 curiosity bills of $1.08B (+10.1% QoQ/ +1.1% YoY), the tobacco firm stays sufficiently worthwhile, with an bettering curiosity protection ratio of 11.33x towards its 5Y common of 10.29x and sector median of seven.54x.

With a debt to EBITDA ratio of two.1x (-0.1x QoQ/ inline YoY) by the most recent quarter, we consider that MO stays well-positioned to navigate the unsure macroeconomic outlook, whereas sustainably rising its dividend at an estimated FWD charge of +4.21% in comparison with its historic charge of +3.79%.

MO’s Future Lies In The Various Tobacco Market

We additionally consider that there’s a future within the e-cigarette segments, with the CDC just lately reporting an immense improve in US gross sales by +47% between January 2020 and December 2022.

The identical has been reported by a number of tobacco firms, specifically Philip Morris (PM), with 27.4M world IQOS customers as of September 2023 (+0.2M QoQ/ +3.7M YoY).

This has contributed to PM’s sustained development within the Heated Tobacco Items bought volumes to 32.47M (+3.3% QoQ/ +18% YoY) and Complete smoke-free merchandise revenues (together with nicotine oral merchandise) to $3.23B (+4.1% QoQ/ +35.7% YoY) by the most recent quarter.

British American Tobacco p.l.c. (BTI) has additionally recorded glorious outcomes, with its New Classes’ development charge nicely exceeding its friends at H1’23 revenues of £1.65B (+26.6% YoY), increasing at an accelerated CAGR of +32.8% from H1’19 levels of £531M.

Most significantly, the tobacco firm’s detailed breakdown of New Classes suggests rising demand for Vapour and THP merchandise, additional validating the continuing transition from typical combustibles.

For now, MO’s various tobacco trajectory has solely been delayed by the earlier Juul fiasco, with the administration already betting on NJOY instead vaping technique.

For now, the tobacco firm experiences a FQ3’23 transport quantity of roughly 7.5M ACE pods (no QoQ/ YoY comparability out there). With the acquisition solely accomplished in June 2023, we consider that it might be extra prudent to offer the administration extra time to combine NJOY into its present operations.

That is particularly since MO’s transformation plan will solely be accomplished by the top of 2023, with the administration anticipating NJOY’s ACE to achieve 70K shops, up by +66% from the present 42K shops by September 2023 and by +103.4% pre-merger of roughly 10K retailer.

The administration has additionally performed its first retail NJOY commerce program, additional increasing the model’s engagement with a number of retail companions, with the hopes of accelerating model consciousness amongst customers.

With NJOY nonetheless in its early days, we consider that it might be prudent to offer MO just a little extra time throughout this transitionary interval, with “the retail share of ACE pods in U.S. multi-outlet and comfort shops nonetheless primarily unchanged because the completion of the NJOY Transaction.”

That is based mostly on the Nielsen convenience store report, with NJOY’s market share remaining considerably steady at 2.5% for the 4 weeks ending October 07, 2023, with the MoM lack of -0.1 level attributed to the BTI Vuse’s rising share to 41.8% (+0.1 factors MoM) as Juul’s share decline to 24.4% (-0.3 factors MoM).

So, Is MO Inventory A Purchase, Promote, Or Maintain?

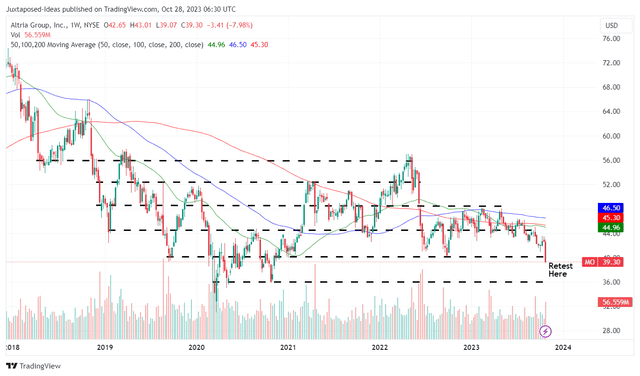

MO 5Y Inventory Value

Buying and selling View

For now, MO has drastically plunged after the current FQ3’23 earnings name, with the inventory retesting its vital assist ranges at $39s/ $40s.

It stays to be seen if bullish assist might materialize right here, because the inventory’s decrease lows and decrease highs because the February 2023 peak might set off an additional retracement to its subsequent assist stage of $36s.

Nevertheless, we consider that lots of long-term MO shareholders might welcome this dip as an opportunity to greenback price common, whereas equally having fun with an expanded ahead dividend yield of 9.97% in comparison with its 5Y common of seven.62% and the sector median of two.88%

As well as, we consider that lots of the readers have been lengthy conscious of the declining typical tobacco gross sales over the previous few a long time, with the vape/ pod/ oral nicotine pouches (amongst others) possible being the next-gen tobacco merchandise.

On account of the continuing transition, we consider that the MO inventory (together with most tobacco shares) is simply appropriate for revenue oriented traders with increased danger tolerance, whom need to purchase and drip indefinitely.

With losses solely realized if the inventory is traded or bought, long-term traders would have merely loved a constant dividend payout each quarterly, irrespective of the noise within the inventory market.