A businessman places cash into his go well with pocket. Ljupco/iStock through Getty Photographs

The legendary supplemental insurer Aflac (NYSE:AFL) is an ideal instance of two the explanation why dividend development investing is my predominant investing technique. With out additional ado, let’s elaborate on that assertion.

When Aflac shared its third-quarter earnings on Nov. 1, it dropped an enormous, stunning bombshell on shareholders: The corporate boosted its quarterly dividend per share by a whopping 19% to $0.50. Placing this into perspective, I used to be solely anticipating a 4.8% elevate to $0.44!

So, for one, superb companies like Aflac can wildly exceed your expectations for dividend development. Secondly, the place else are you going to get a 19% elevate?

Out of your day job? When you pour your coronary heart and soul into it, possibly you will get that profitable promotion. However even then, it is fairly unlikely that you will get that massive of a pay elevate. The very best half is that merely proudly owning shares in nice companies requires little or no effort. Past the preliminary part of securing capital to spend money on such a enterprise and infrequently checking in on fundamentals, there is not any work to be finished.

Since my earlier article on Aflac in October, let’s reassess the corporate’s fundamentals and valuation to spotlight why I’m retaining my maintain score for now.

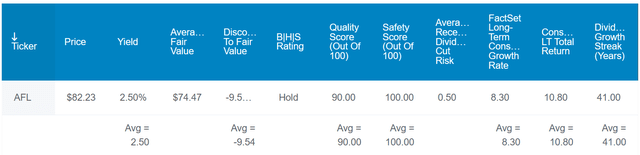

DK Zen Analysis Terminal

Aflac and its 2.5% dividend yield could not have the ability to bathe you with enormous beginning passive earnings. However the Dividend Aristocrat makes up for this decrease earnings with a really secure 31% EPS payout ratio. That is effectively underneath the 50% that score companies view as sustainable for insurers per Dividend Kings.

Aflac can also be a financially sound enterprise. The corporate’s 19% debt-to-capital ratio is slightly below the 20% that score companies contemplate to be strong. Maybe it is no shock then that Aflac’s company credit standing is A- from S&P on a steady outlook. This indicators that the danger of the corporate not being round in 2053 is merely 2.5%.

DK Zen Analysis Terminal

The one factor I do not notably like about Aflac proper now’s its valuation. A mean of Dividend Kings’ truthful values peg Aflac to be price $74 a share, which is 9% lower than the present $81 share value (as of November 10, 2023).

My truthful worth estimate utilizing the dividend low cost mannequin is $73 a share, which is 12% above the present share value. I arrived at this truthful worth through the use of the annualized dividend per share of $2, a ten% low cost charge, and a 7.25% annual dividend development charge for the lengthy haul.

Averaging these truthful values collectively, I get a good worth of about $74 a share. Assuming Aflac meets the analyst development consensus and returns to truthful worth, these are the entire returns the corporate might ship within the coming 10 years:

- 2.5% yield + 8.3% FactSet Analysis annual earnings development consensus – 1% annual valuation a number of contraction = 9.8% annual whole return potential or a 155% cumulative whole return versus the ten% annual whole return prospects of the S&P 500 (SP500) or a 160% cumulative whole return

A Sturdy Third-Quarter Displaying

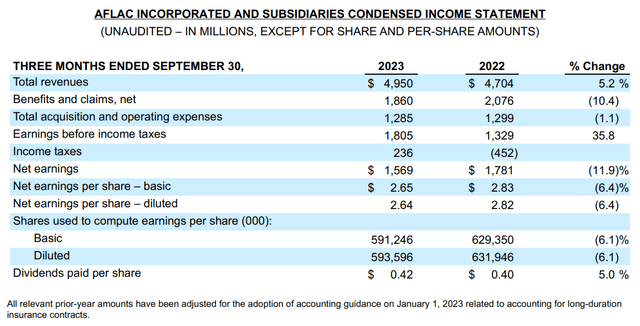

Aflac Q3 2023 Earnings Press Launch

As stockalien within the Searching for Alpha group put it with a clockwork pun, Aflac is like quackwork. Seeing as Aflac’s income grew by 5.3% year-over-year to $5 billion throughout the third quarter, I could not agree extra with this evaluation. For extra coloration, this beat the analyst consensus by a staggering $500 million.

These outcomes have been principally attributable to a big uptick in web funding features, which greater than doubled to $514 million within the third quarter. This was largely attributable to a overseas forex acquire from the weakening Japanese Yen (pages 20 and 26 of 129 of Aflac 10-Q filing).

The opposite issue that helped Aflac a 3.9% development charge in Aflac U.S. adjusted income to $1.7 billion for the third quarter. Regular underlying demand for its merchandise and development initiatives of group life and incapacity and community dental and imaginative and prescient contributed to this development per Chairman and CEO Dan Amos’ opening remarks throughout Aflac’s Q3 2023 earnings name.

Aflac Japan’s adjusted income fell 4.9% over the year-ago interval to $2.7 billion throughout the third quarter. This is not what it appears, although. The section’s currency-neutral gross sales grew by 12.4%, which was led by double-digit development in most cancers insurance coverage gross sales. This income decline was solely due to the Yen’s unfavorable overseas change charge versus the U.S. Greenback.

Aflac’s currency-neutral adjusted diluted EPS soared 31.9% year-over-year to $1.90 for the third quarter. Moreover the next income base, the corporate’s surging income have been fueled by margin growth. Aflac US recorded a pretax adjusted revenue margin of 28.8% (it was 21.6% within the year-ago interval) and Aflac Japan posted a 32.8% pretax adjusted revenue margin (versus 29.3% within the year-ago quarter). A 6.1% discount within the firm’s excellent share depend attributable to share repurchases additionally performed an element within the a lot larger currency-neutral adjusted diluted EPS.

As you’d anticipate for a well-run insurer, Aflac’s capital construction is kind of conservative as effectively. The corporate had $111.3 billion in investments and money as of Sept. 30 versus simply $86 billion of estimated coverage liabilities (particulars in earlier paragraphs in line with Aflac Q3 2023 earnings press release).

The Dividend Can Preserve Transferring Increased

Accounting for Aflac’s upcoming quarterly dividend per share, its dividend has grown by 85% in simply the final 5 years. Whereas I would not anticipate that a lot development over the following 5 years, I nonetheless imagine respectable dividend development lies forward.

By the primary 9 months of 2023, Aflac generated $2.4 billion in free money stream (per web page 10 of 129 of Aflac 10-Q submitting). Towards the $730 million in dividends paid throughout this time, that’s only a 31% free money stream payout ratio. This leaves loads of room for the dividend to proceed rising.

Dangers To Contemplate

Aflac is a outstanding firm with a monitor report that is robust to beat. Nevertheless, it nonetheless has dangers that buyers should tolerate.

As I mentioned in my earlier article, two of probably the most notable dangers are the focus of income and property in Japan, and Aflac’s dependence on face-to-face interplay to conduct its operations.

Moreover, the corporate faces underwriting danger as an insurer. If morbidity and mortality considerably differ from Aflac’s expectations, the corporate’s monetary outcomes could possibly be damage.

Abstract: The Proper Entry Level Might Be Very Worthwhile

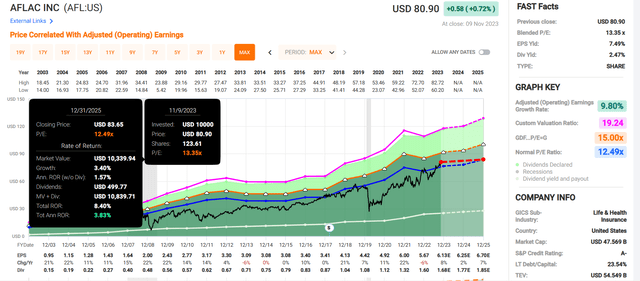

FAST Graphs, FactSet

Aflac’s fame of 4 consecutive a long time and counting of dividend development places it within the dialog of being an elite enterprise. However I reside by the philosophy of Warren Buffett to purchase fantastic companies round or beneath truthful worth.

Sadly, Aflac seems to be priced a bit past its truthful worth. In response to FAST Graphs, the inventory’s 13.4 blended P/E ratio is larger than its regular P/E ratio of 12.5. Taking this into consideration, Aflac could solely ship 4% annual whole returns by means of 2025 if it reverts to truthful worth. On the proper valuation, Aflac might beat the market. However because it stands with the present valuation, it’s going to have a troublesome time doing so. That’s why I charge it a maintain.