deepblue4you

Together with JPMorgan (JPM) reporting their calendar This fall ’23 monetary outcomes, on Friday morning, January twelfth, 2023, Citigroup (C) and Financial institution of America (BAC) will achieve this as effectively.

Having by no means lined or modeled Wells Fargo (WFC) for any time period, regardless that they too will report Friday morning, the earnings won’t be lined right here.

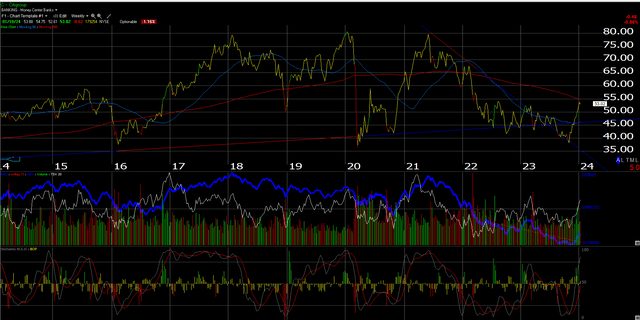

Citigroup

Citigroup is a darling of world-class worth traders like Invoice Nygren of Oakmark and Warren Buffett’s Berkshire Hathaway, and when each famous they had been shopping for the inventory, I took an curiosity and purchased some as effectively.

Mike Mayo, the legendary financial institution analyst now at Wells Fargo, has come out within the final two weeks on a CNBC look and put a worth goal on Citi of $80 per share, which might be a doubling of the inventory worth from the late October ’23 lows.

With all due respect to Mayo although, Citi has traded as much as $80 in early 2018, early 2020, after which in early June ’21, in response to this weekly chart:

The one distinction to the above sample is that it’s taking up 2.5 years to start out its transfer again as much as $80 per share, though 2021’s bounce was tremendously aided by ZIRP (zero rate of interest coverage) and the capital markets.

Principally, Mike is looking for the ball to bounce once more, though a everlasting enchancment in fundamentals may assist drive the rise, versus momentary components.

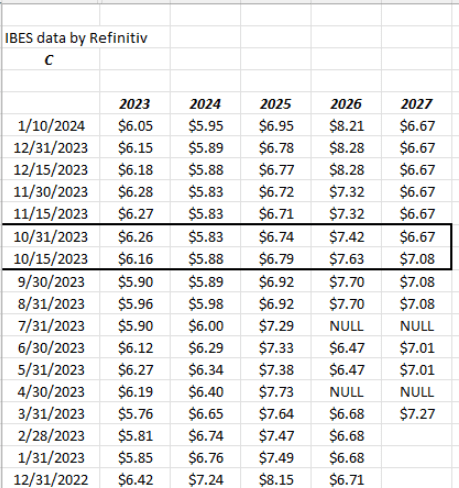

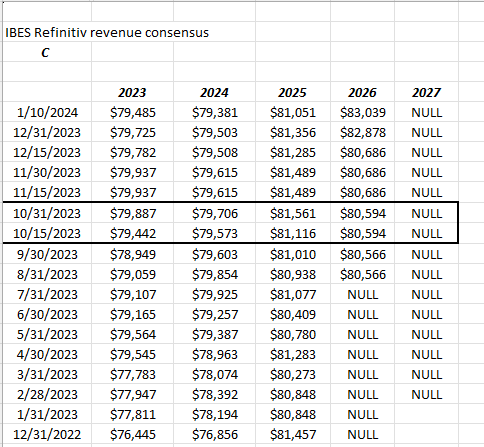

EPS and income estimate revisions:

The Citi EPS estimate revisions confirmed an enchancment after October ’23’s earnings had been launched, significantly for 2023, however have now settled again in December ’23, whereas 2024 and 2025 work greater.

Jane Fraser, Citi’s CEO, has already introduced some payroll or workers downsizing, and in addition has introduced that Citi will exit the municipal bond business, which is able to influence one other 100 workers.

What no person’s saying is that – at the very least in response to my spreadsheet which exhibits the variety of Citi workers each quarter, Citi had 240,000 full-time workers as of the tip of Q3 ’23, which is up 20,000 from the 220,000 on the finish of September ’21.

Possibly Citi’s plan is just to scale back the current hires.

Citi income revisions have turned optimistic since earlier in ’23, however have slid again for the reason that October ’23 earnings report.

Valuation: With the inventory buying and selling at simply 9x ’23 earnings with a dividend yield slightly below 4%, (and the dividend hasn’t been elevated since 2019), and a price-to-tangible guide of 0.6x, the inventory has appeared low-cost for years, however the well-below-average ROE of seven%, lags its peer group materially.

Income progress anticipated between ’24 and ’26 is simply 1% common over the 3-year interval.

Jane Fraser will doubtless be pressed to proceed to enhance ROE and ROA, with out chopping bone.

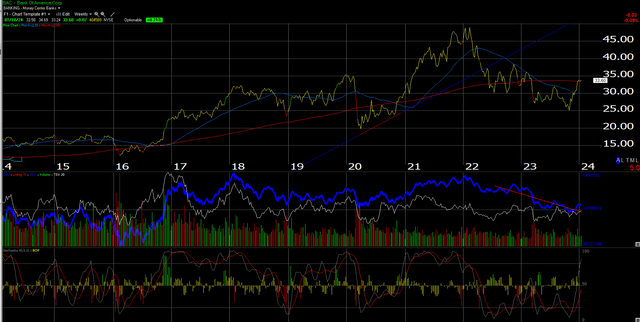

Financial institution of America

Financial institution of America gave the impression to be damage by less-than-robust web curiosity revenue in early ’23, and never having the ability to capitalize on greater rates of interest in both the funding or mortgage portfolios.

Because the above weekly chart exhibits, BAC traded beneath the 50 and 200-week transferring averages however has now climbed again above the 200-week transferring common, very just lately.

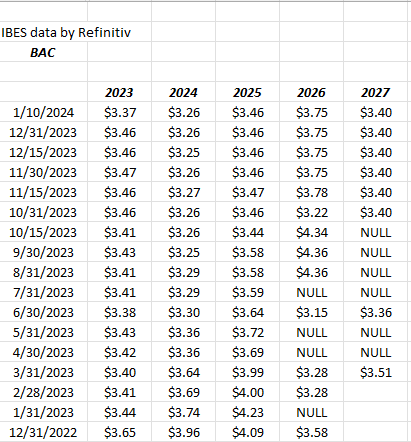

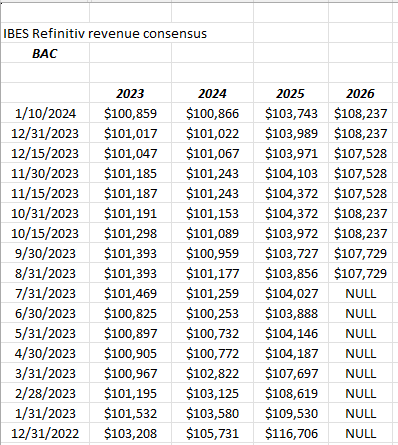

BAC EPS and income estimate revisions:

EPS estimates have been steadily decrease since early ’23. Not very encouraging.

BAC income revisions have additionally seen a gentle slide since late 2022, early 2023. These estimate revisions too aren’t very encouraging.

Valuation: BAC is anticipating an “common” of two% income progress and three% EPS progress from 2024 to 2026 because the consensus estimates stand right now, which like the opposite banks, doesn’t look that nice.

Buying and selling at 9-10x present earnings and at 1x guide, and 1.2x tangible guide, the valuation is hardly costly, however all this is sensible with the anticipated progress.

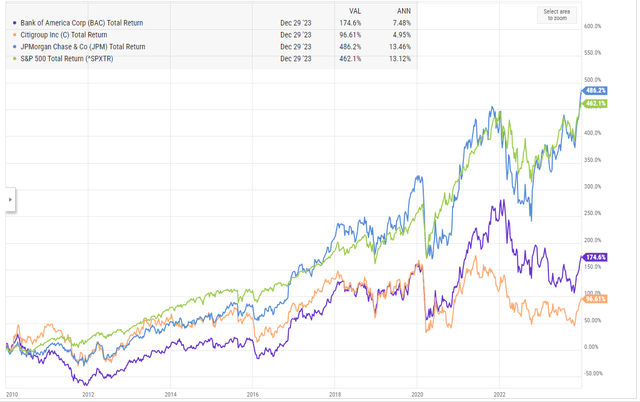

Relative efficiency versus the S&P 500:

This graph exhibits JPMorgan, Citi and Financial institution of America benchmarked in opposition to the S&P 500, since 1/1/2010.

JPMorgan is the one inventory of the three to beat the S&P 500 within the final 13 years.

Abstract:

Anticipated EPS progress: 2024-2026:

- JPM: -2% (go determine)

- BAC: 2%

- C: 11%

Anticipated income progress 2024-2026:

- JPM: -1% (once more, it’s the maths)

- BAC: 2%

- C: 1%

Present P/E avg (2024-2026):

Value-to-tangible guide worth:

- JPM: 1.80x

- BAC: 1.20x

- C: 0.60x

ROE/ROTCE:

- JPM: 15% – 17%

- BAC: 14%

- C: 6% – 7%

Mr. Buffett constantly sings Brian Moynihan’s praises (Financial institution of America CEO), however the inventory has generated solely half the return of JPM and the S&P 500 since 1/1/2010.

For me, and it’s one opinion, JPM and C characterize the proper mixture of “earnings progress” and “guide worth”. Shoppers are lengthy some BAC however the inventory appears to languish in each good and unhealthy rate of interest environments.

Nonetheless, readers might stay lengthy BAC and in the end await the catalyst that strikes the inventory greater.

I do assume all three shares might win with a return to a standard yield curve (i.e. longer Treasury yields above shorter Treasury yields).

None of that is recommendation or a advice. These write-ups are executed to make clear my very own pondering and to make sure I’ve gone by the self-discipline of operating the numbers.

Previous efficiency isn’t any assure and even suggestion of future outcomes. Capital markets change rapidly, for each the nice and the unhealthy. Watch out for rotation.

Readers ought to gauge their very own consolation stage with portfolio volatility and alter accordingly. IBES knowledge by Refinitiv is the supply for EPS and income estimates.

Thanks for studying.

Editor’s Notice: The abstract bullets for this text had been chosen by In search of Alpha editors.