JHVEPhoto

As a substitute Of An Funding Thesis

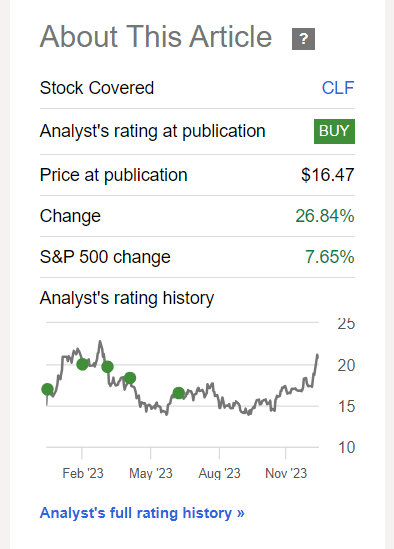

I have been masking Cleveland-Cliffs Inc. (NYSE:CLF) inventory since June 2021, and all alongside I have been bullish on the inventory for a lot of causes. The final time – in June 2023 – I argued for a severe undervaluation of the corporate in mild of its superior projected progress charges in FY2024-25 and implied multiples which might be nicely beneath these of its peer group. Since then, CLF has managed to considerably outperform the broad market, displaying ~27% in return:

In search of Alpha, Oakoff’s earlier article on CLF

And primarily based on what I see at this time, my thesis hasn’t modified: I nonetheless see a better share value for CLF over the following few years, making it an excellent long-term ‘Purchase’ at this time.

My Reasoning

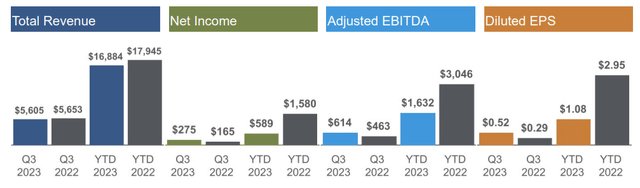

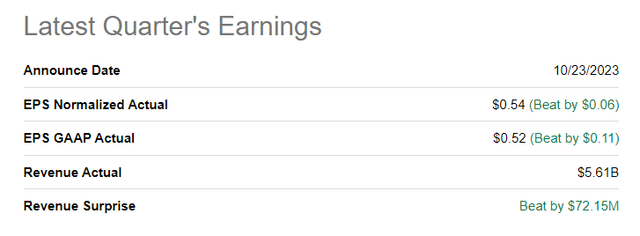

In Q3 FY2023, Cleveland-Cliffs reported revenues of $5.6 billion, with adjusted EBITDA of $614 million and GAAP EPS of $0.52. Regardless of the UAW strike affecting 3 automotive shoppers, complete shipments reached 4.1 million web tons, setting a quarterly report for metal shipments to the automotive sector. On the similar time, CLF’s value discount efficiency was robust, enhancing by $31 per web ton in Q3. So though the YoY dynamics in gross sales have been flat, the margins went up considerably in the course of the interval:

CLF’s 10-Q

Consequently, CLF beat the bottom-line consensus forecast:

In search of Alpha

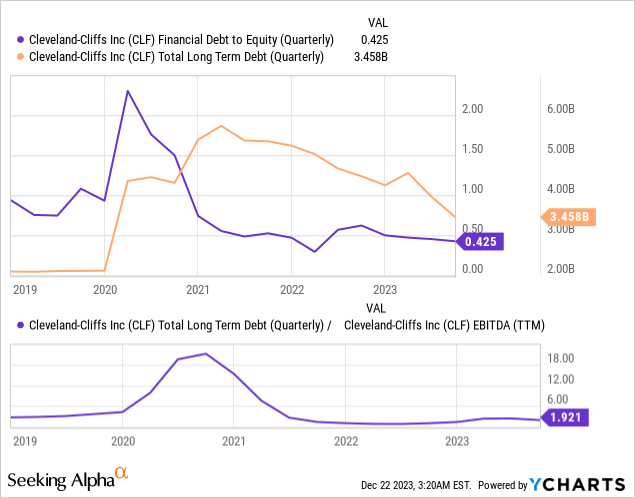

The agency’s free money movement for the quarter amounted to $605 million, primarily used to pay down the ABL, lowering web debt to $3.4 billion and growing complete liquidity to $4.4 billion. So CLF’s debt-to-equity decreased additional in Q3, and the debt-to-EBITDA received beneath 2x:

The corporate’s capital construction is now primarily comprised of low-cost fastened coupon debt devices, with no upcoming maturities till 2026. Since buying ArcelorMittal USA in December 2020, CLF has decreased web debt by almost $2 billion and eradicated $3.5 billion in pension and OPEB liabilities.

Except for the debt discount, CLF purchased again 3.9 million shares, returning ~$60 million to shareholders. That is ~0.56% of at this time’s market capitalization, however I consider it is a short-term quantity as the corporate turns into extra versatile on share buybacks because it reduces its debt load.

Throughout Q3 FY2023 Cleveland-Cliffs was in a position to keep robust common promoting costs above $1,200 per web ton. Now value discount is predicted to proceed, in keeping with the administration’s feedback in the course of the newest earnings name, with a further $15 per web ton discount forecasted for This fall.

CLF additionally highlighted its place within the automotive market, emphasizing excellence in assembly buyer wants. They anticipate complete shipments in This fall to stay at ~4 million web tons, even when the UAW strike persists. The impression of the strike on CLF appears to be much less important than earlier challenges such because the microchip scarcity and different provide chain points.

The corporate’s dedication to purchasing a good portion of the output from a clear hydrogen hub in northwest Indiana helped secure the location in October 2023.

As for the failed buy of United States Metal (X), which is finally going to be bought to the Japanese firm Nippon Metal (OTCPK:NPSCY), CLF shareholders have truly benefited from that end result: The corporate is not going to should tackle extra debt, which might additional diminish the prospects of accelerating shareholder returns indefinitely. Name me short-sighted, however as a shareholder of the corporate, I need it to do away with the debt as quickly as doable, whereas it’s doable because of the nonetheless robust financial system. The merger with X might have come on the mistaken time, destroying worth for shareholders and making CLF extra weak in a doable turbulent financial interval (that will be a consequence of the excessive stakes anyway; it is a matter of timing, in my view).

Now the corporate can proceed to boost metal costs with none extra burden, because it did once more not too long ago, thus sustaining margins and benefiting from the nonetheless low automobile inventories within the US, which must be replenished in any case.

TradingEconomics, Home Automotive Inventories

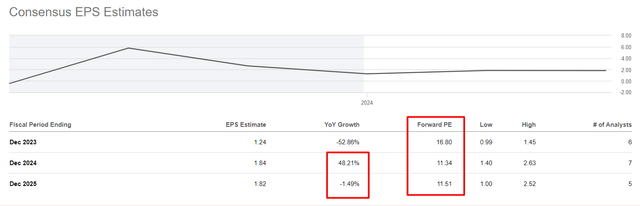

CLF, which has one of many dominant roles within the metal {industry} with a concentrate on automakers, continues to be virtually as low cost as after I checked out it in June 2023. Sure, the P/E ratio for FY2025 seems to be larger than earlier than, however the EPS progress forecasts for that yr predict stagnation.

In search of Alpha, creator’s notes

I can not agree with that consensus, because the agency’s debt ought to proceed to fall and buybacks ought to improve by then – each of which have a constructive impression on EPS on a YoY foundation.

Dangers To Take into account

I need everybody studying this text to take into account that investing in CLF shares carries a number of dangers that should be rigorously weighed. First, market threat is ever-present, as the worth of the inventory depends upon basic market situations and geopolitical occasions. As CLF is linked to the metal and iron ore {industry}, buyers are uncovered to industry-specific challenges similar to demand fluctuations, iron ore value volatility, and aggressive pressures. Monetary stability and administration effectiveness additionally contribute to the danger profile, with elements similar to debt and operational challenges probably impacting share efficiency. Commodity value threat is a key issue as CLF is energetic in mining and metal manufacturing. Fluctuations in international commodity costs can subsequently have a big impression on the corporate’s revenues and profitability, which represents a further uncertainty for the funding. Regulatory and political dangers, each at nationwide and worldwide ranges, might also have a adverse impression on CLF’s enterprise actions.

Your Takeaway

Regardless of all of the dangers, CLF inventory continues to be considered one of my favourite firms within the {industry}. The corporate is recovering in seemingly robust instances and with a number of headwinds. So simply take into consideration what potential the corporate might need in calm instances.

I additionally suppose the share value continues to be low cost. It is nonetheless a ‘discount’ as buyers say, and do not be delay by some excessive TTM multiples because the FWD multiples present a really totally different image. From all this, I conclude that it nonetheless is smart to carry CLF in a long-term portfolio and to proceed shopping for on the present value degree, although it is up +24.5 % year-to-date.

Good luck together with your investments!

Editor’s Observe: This text discusses a number of securities that don’t commerce on a significant U.S. alternate. Please concentrate on the dangers related to these shares.